Key Events In The Coming Busy Week: Jobs, PMIs, And Central Banks

Key Events In The Coming Busy Week: Jobs, PMIs, And Central Banks Tyler Durden

Mon, 11/30/2020 – 09:39

With just a handful of trading days left until the end of what has been an absolutely insane 2020, it’s shaping up to be a fairly busy week for data but as DB’s Jim Reid writes, “how much markets will care is a moot point as everyone knows we’re on a short-term path to a double dip but that the short to medium term is a path covered in potential golden vaccine petals.”

Data releases include the US jobs report (Friday) and the November PMIs (tomorrow and Thursday), while Fed Chair Powell and ECB President Lagarde will both be speaking through the week. Otherwise, attention will remain on the Brexit negotiations, with just a month remaining until the year-end deadline and less time given any deal has to be ratified across the continent.

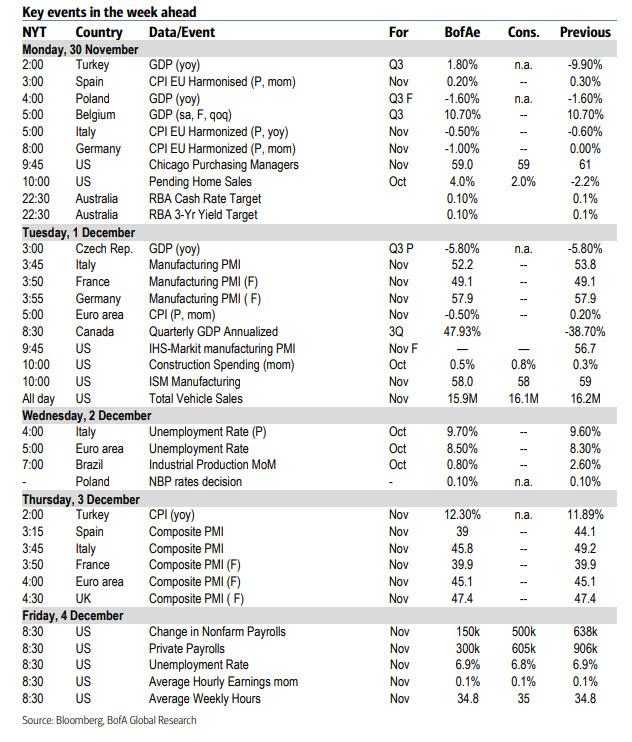

A full breakdown of key events is shown below:

Looking into more detail, the US jobs report for October on Friday sees consensus at +500k and a fall in the unemployment rate to 6.8% from 6.9%. Though this would be further progress from the situation in the spring, it would still be the slowest monthly jobs growth since the massive contractions in March and April, and leave the total nonfarm payrolls number over 9.5m beneath its pre-Covid peak back in February. Of some concern is the recent weekly initial jobless claims trend which have risen more than expected for the last couple of weeks. So it feels like a difficult month or so ahead for the US economy.

Meanwhile on the PMIs, the flash readings we’ve already had showed a noticeable deterioration in Europe as much of the continent headed into renewed lockdowns. It’ll be interesting to gauge what’s happening in the countries where there aren’t flash readings however, including a number of emerging markets. Also in focus will be the Euro Area’s flash CPI estimate for November tomorrow as for the previous 3 months it’s been in deflationary territory.

Elsewhere on Brexit, face to face talks are back with we are running low on days to ratify a deal. In terms of the current state of play, it has been reported that the last big remaining obstacle in the talks is fishing rights with the UK Foreign Secretary Dominic Raab asking the EU to recognize that regaining control over British waters is a question of sovereignty for the UK. Meanwhile, on other key obstacles of competition rules and state aid, Raab said that he could see “a landing zone”. If fishing is truly now the only stumbling block this is very good news as the numbers here are minuscule compared to the cost of no deal. Sterling is up +0.21% to 1.3339 overnight.

Finally, there are a number of important central bank speakers this week, with Fed Chair Powell and Treasury Secretary Mnuchin appearing before the Senate Banking Committee tomorrow and the House Financial Services Committee on Wednesday. Meanwhile ECB President Lagarde will be speaking today at the European Policy Center Forum, before she appears at an Atlantic Council event tomorrow. The Fed will also be releasing their Beige Book on Wednesday.

Below, courtesy of Deutsche Bank, here is a day-by-day calendar of events

Monday November 30

Data: China November composite, manufacturing and non-manufacturing PMIs, Japan October housing starts, UK October mortgage approvals, Italy preliminary November CPI, Germany preliminary November CPI, Canada October building permits, US November MNI Chicago PMI, Dallas Fed manufacturing index, October pending home sales, Japan October jobless rate (23:30UK time)

Central Banks: ECB President Lagarde and BoE’s Tenreyro speaks

Tuesday December 1

Data: November Manufacturing PMIs from Indonesia, South Korea, Japan, China, India, Russia, Turkey, Italy, France, Germany, South Africa, Euro Area, UK, Brazil, Canada, US and Mexico, Japan November vehicle sales, Germany November unemployment change, Euro Area November flash CPI estimate, Canada September GDP, US November ISM manufacturing

Central Banks: Fed Chair Powell, ECB President Lagarde and the Fed’s Brainard, Daly and Evans speak, Reserve Bank of Australia monetary policy decision

Other: OECD publishes Economic Outlook

Wednesday December 2

Data: Euro Area October unemployment rate, US weekly MBA mortgage applications, November ADP employment change

Central Banks: Federal Reserve releases Beige Book, Fed Chair Powell and Fed’s Williams speak

Thursday December 3

Data: November services and composite PMIs from Japan, China, India, Russia, Italy, France, Germany, Euro Area, UK, Brazil and the US, Euro Area October retail sales, US weekly initial jobless claims, November ISM services index

Central Banks: Fed’s Bowman and BoE’s Tenreyro speak

Friday December 4

Data: Germany October factory orders, November construction PMI, Italy October retail sales, UK November construction PMI, Canada November net change in employment, US November nonfarm payrolls, unemployment rate, average hourly earnings, October trade balance, factory orders, final October durable goods orders, nondefence capital goods orders ex air

Central Banks: Reserve Bank of India monetary policy decision

Finally, looking at the US alone, the key economic data releases this week are the ISM manufacturing report on Tuesday, ISM non-manufacturing report and jobless claims on Thursday, and the employment report on Friday. There are several speaking engagements from Fed officials this week, including Chair Powell on Tuesday and Wednesday. Here is Goldman’s take on what to expect:

Monday, November 30

09:45 AM Chicago PMI, November (GS 60.1, consensus 59.1, last 61.1); We estimate that the Chicago PMI edged down by 1.0pt to 60.1 in November. Our forecast reflects resilience in the manufacturing sector.

10:00 AM Pending home sales, October (GS -1.5%, consensus +1.0%, last -2.2%): We estimate that pending home sales declined by 1.5% in November, reflecting a further deceleration in regional home sales data.

Tuesday, December 1

09:45 AM Markit Flash US manufacturing PMI, November final (consensus 56.7, last 56.7)

10:00 AM ISM manufacturing index, November (GS 58.3, consensus 57.8, last 59.3): We expect the ISM manufacturing index to edge down by 1.0pt to 58.3 in the November report, reflecting resilience in the manufacturing sector. Our GS Manufacturing Tracker stands at 57.2 in November, compared to 58.2 in October.

10:00 AM Construction spending, October (GS +1.0%, consensus +0.8%, last +0.3%): We estimate a 1.0% increase in construction spending in October, with scope for increases in private residential and public construction.

10:00 AM Fed Chair Powell (FOMC voter) speaks: Fed Chair Powell will appear before the Senate Banking Committee to discuss the CARES Act. Prepared text is expected.

12:00 PM Fed Governor Brainard (FOMC voter) speaks: Fed Governor Brainard will take part in an online discussion of the modernization of the Community Reinvestment Act. Prepared text and moderated Q&A are expected.

01:15 PM San Francisco Fed President Daly (FOMC non-voter) speaks: San Francisco Fed President Daly will speak at a virtual economic forecast luncheon hosted by Arizona State University. Prepared text and Q&A with audience and media are expected.

03:00 PM Chicago Fed President Evans (FOMC non-voter) speaks: Chicago Fed President Evans will make opening remarks at a community forum on Milwaukee’s future hosted by the Chicago Fed.

Wednesday, December 2

08:15 AM ADP employment report, November (GS 525k, consensus 440k, last 365k); We expect a 525k gain in ADP payroll employment, reflecting a decline in jobless claims and firmness in private payrolls in November.

10:00 AM Fed Chair Powell (FOMC voter) speaks: Fed Chair Powell will appear before the House Financial Services Committee to discuss the CARES Act. Prepared text is expected.

01:00 PM New York Fed President Williams (FOMC voter) speaks: New York Fed President Williams will brief the press on the economic impact of Covid-19. Prepared text is not expected.

Thursday, December 3

08:30 AM Initial jobless claims, week ended November 28 (GS 760k, consensus 765k, last 778k); Continuing jobless claims, week ended November 21 (consensus 5,811k, last 6,071k):We estimate initial jobless claim decreased to 760k in the week ended November 28. Our forecast assumes that the worse virus situation continues to put upward pressure on initial claims, but that the DOL’s seasonal adjustment understates the decline in filings due to the Thanksgiving holiday.

09:45 AM Markit Flash US services PMI, November final (consensus 57.6, last 57.7)

10:00 AM ISM non-manufacturing index, November (GS 55.5, consensus 56.1, last 56.6): We estimate the ISM non-manufacturing index declined by 0.6pt to 55.5 in November, reflecting a likely pullback in leisure, food services, and other services. Our GS Non-Manufacturing Tracker stands at 55.2, compared to 56.1 in October.

Friday, December 4

08:30 AM Nonfarm payroll employment, November (GS +450k, consensus +500k, last +638k); Private payroll employment, November (GS +525k, consensus +608k, last +906k); Average hourly earnings (mom), November (GS +0.1%, consensus +0.1%, last +0.1%); Average hourly earnings (yoy), November (GS +4.2%, consensus +4.2%, last +4.5%); Unemployment rate, November (GS 6.8%, consensus 6.8%, last 6.9%): We estimate nonfarm payrolls rose 450k in November after +638k in October. The broad-based resurgence of the coronavirus and related business restrictions are consistent with a deceleration in job growth, and Big Data employment signals were softer on net. While continuing claims declined during the payroll month, much of the drop reflected the expiration of program eligibility (as opposed to reemployment), and initial claims have started rising again. We also expect a 90k drop in Census jobs in Friday’s report. On the positive side, we estimate strong growth in the construction industry and in trucking, courier, and delivery categories, reflecting favorable weather and the accelerating shift to ecommerce this holiday season, respectively.

We estimate the unemployment rate declined a tenth to 6.8%, reflecting an increase in household employment and a pause in the labor force participation rebound (itself related to the third wave of the virus). We estimate average hourly earnings rose 0.1% month-over-month, lowering the year-on-year rate by three tenths to 4.2%. This forecast reflects negative calendar effects and a continuing unwind of the composition shift from lower-paid workers to higher-paid workers.

08:30 AM Trade balance, October (GS -$65.0bn, consensus -$64.8bn, last -$63.9bn): We estimate the trade deficit increased by $1.1bn in October, reflecting an increase in the goods trade deficit. Goods imports have returned to their pre-pandemic level, but monthly goods exports are still about $15bn below their pre-pandemic level. Both imports and exports of services have recovered only slightly from their Q2 troughs.

10:00 AM Factory orders, October (GS +0.7%, consensus +0.8%, last +1.1%); Durable goods orders, October final (last +0.5%); Durable goods orders ex-transportation, October final (last +0.3%); Core capital goods orders, October final (last +0.7%); Core capital goods shipments, October final (last +2.3%): We estimate factory orders increased by 0.7% in October following a 1.1% increase in September. Durable goods orders rose by 1.3% in the October advance report, and core capital goods orders rose by 0.7%.

10:00 AM Fed Governor Bowman (FOMC voter) speaks: Fed Governor Bowman will discuss community banking and fintech in an online event hosted by the Independent Community Bankers of America. Prepared text and moderated Q&A are expected.

{kind=link}