More debt equals less growth. In October, I discussed the “2nd Derivative Effect” and the ongoing cost of the stimulus. With the passage of the $1.9 trillion “American Rescue Plan,” will the math of debt to growth change?

Now, even Deutsche Bank credit strategist, Stuart Sparks, got the memo.

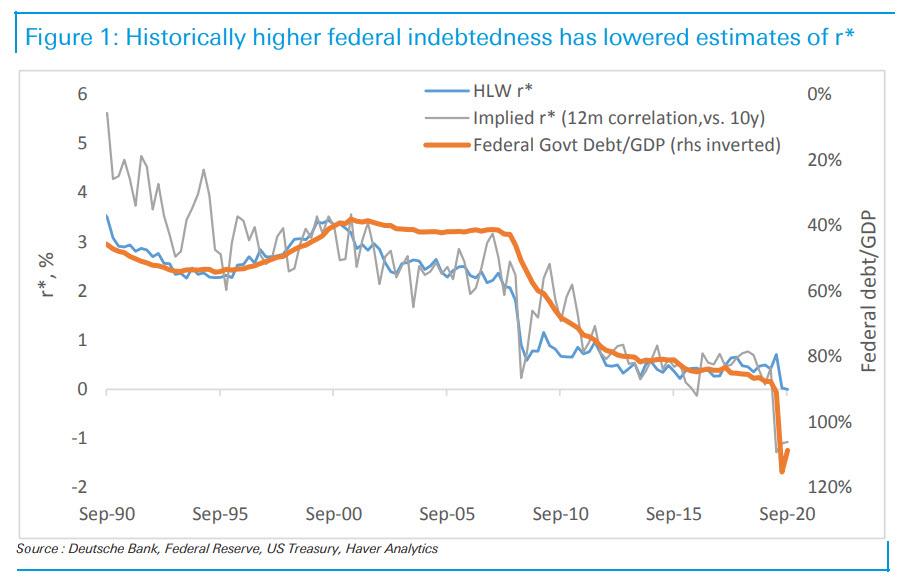

“History teaches us that although investments in productive capacity can in principle raise potential growth and r* in such a way that the debt incurred to finance fiscal stimulus is paid down over time (r-g<0), it turns out that there is little evidence that it has ever been achieved in the past.

The chart below illustrates that a rising federal debt as a percentage of GDP has historically been associated with declines in estimates of r* – the need to save to service debt depresses potential growth. The broad point is that aggressive spending is necessary, but not sufficient. Spending must be designed to raise productive capacity, potential growth, and r*. Absent true investment, public spending can lower r*, passively tightening for a fixed monetary stance.”

Such is a logical conclusion, but one widely dismissed by economists and politicians. However, some fundamental analysis will underscore Mr. Sparks’ comments.

To keep some consistency in the analysis, let’s review the actions to date.

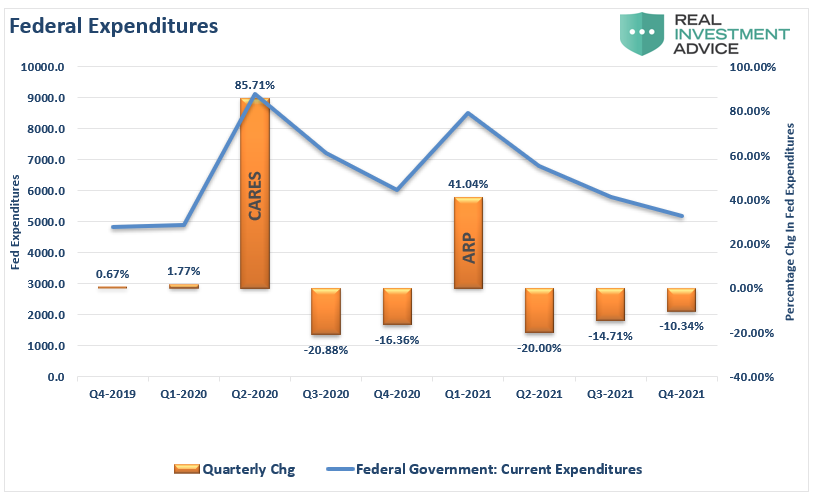

As the economy shut down in March of last year due to the pandemic, the Federal Reserve flooded the system with liquidity. At the same time, Congress passed a massive fiscal stimulus bill that extended Unemployment Benefits by $600 per week and sent $1200 checks directly to households.

In December, Congress passed another $900 stimulus bill extending unemployment benefits at a reduced amount of $300 per week, plus sending $600 checks to households once again.

Now, the latest iteration of Government largesse comes in a solely Democrat supported $1.9 trillion “spend-fest.” Out of the total, only about $900 billion goes to consumers in the form of $400 extended unemployment benefits and $1400 checks directly to households. The remaining $1.1 trillion will have little economic value as bailing out municipalities and funding pet projects doesn’t boost consumption.

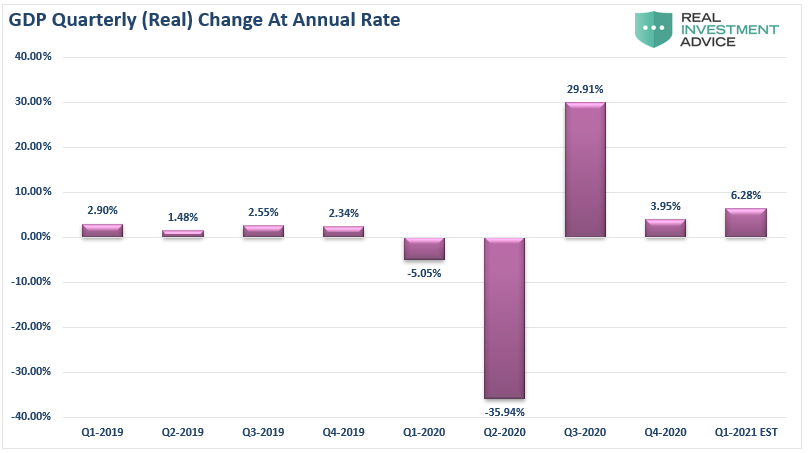

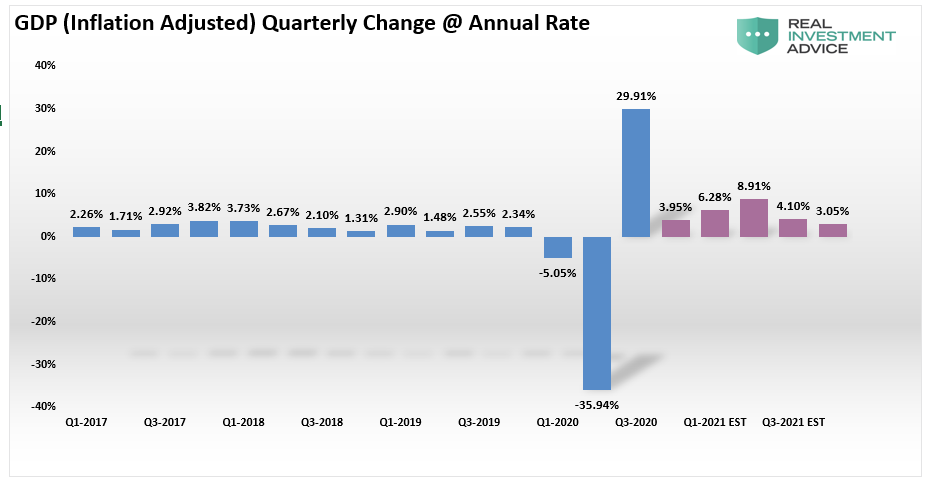

Using current economic data, we can calculate estimates for the estimated impact of the economy’s stimulus through 2021. As shown in the chart below, in Q3, the inflation-adjusted GDP surged 29.91% from the Q2 reading of -35.94%. As stimulus ran out, Q4 GDP only increased by 3.95%. If we assume that Q1 will increase by the Atlanta Fed GDPNow estimate, GDP will show an 6.2% advance. That advance is the result of the $900 billion stimulus bill in December.

If we assume the next round of direct checks to households hit by April, GDP will rise by 6.67% in the second quarter. In other words, the “2nd derivative effect” of a larger economy reduces the rate of change from the stimulus and its ability to create growth.

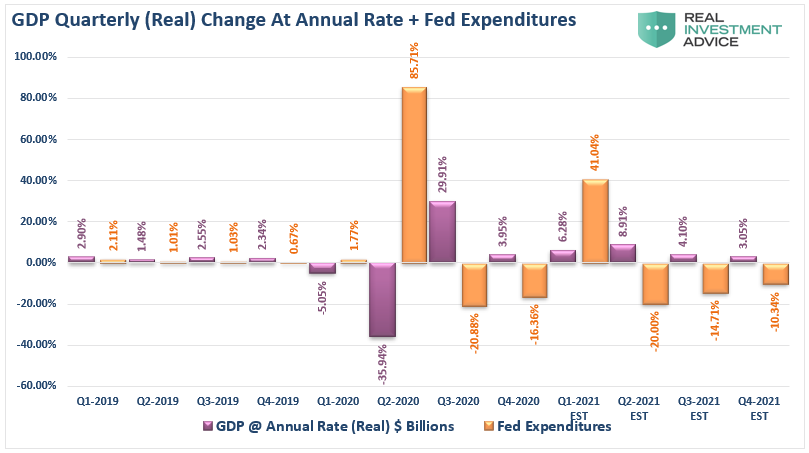

The chart below adds the percentage change in Federal expenditures to the chart for comparison. The 41% jump in expenditures in Q1 is from the combined $900 billion and 1/3rd of the latest stimulus bill. The remainder of the newest bill is then spread into Q2 and ending in Q3 of 2021. At such time Federal spending is assumed to return to is $4.5 trillion quarterly run rate.

We will revise these estimates as data becomes available. However, based on previous stimulus bills’ impact, we have a relatively high degree of confidence in our forecasts.

Economists estimate the latest stimulus bill could add nearly $1 trillion to nominal growth (before inflation) during 2021. While such a surge in growth would be welcome, it represents just $0.50 of growth for each dollar of new debt.

Such a high growth estimate also assumes that individuals will quickly spend their checks in the economy. The hope is that as vaccines become available, individuals will unleash their “pent-up” demand from the last year.

While that could indeed be the case, there are also other facts to consider.

For example, following the initial stimulus bill’s passage, following the shutdown of the economy, many workers assumed their job loss was temporary. However, a year later, unemployment remains high, and many temporary layoffs have become permanent. Such may well change individuals’ spending behavior, leading them to pay off debt, back rent, late mortgage payments, or save just in case employment remains elusive.

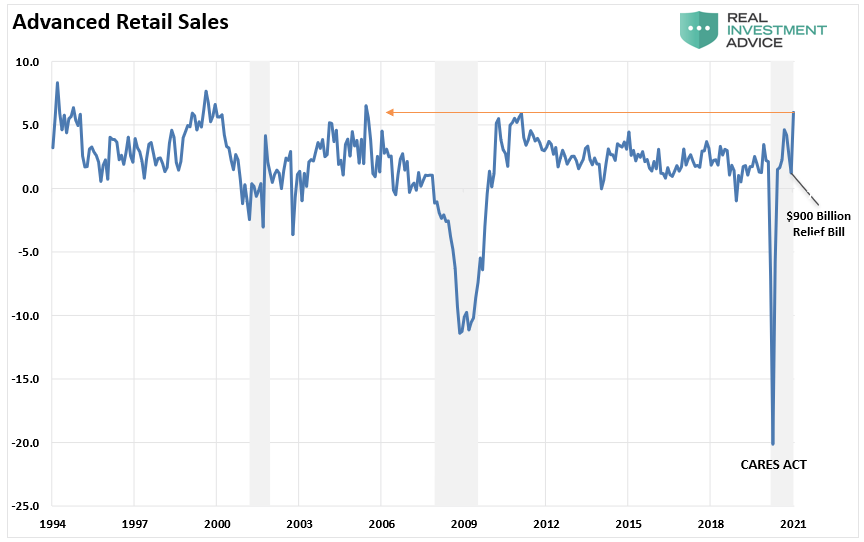

Furthermore, much of the “pent up” demand was already pulled forward by the previous two stimulus plans. We have already witnessed robust increases in manufacturing and services data suggesting consumers have been at work spending money over the last few quarters. The recent surge in retail sales confirms the same.

As discussed previously, while the next American Rescue Plan will be roughly the same size as the original CARES Act, its impact on the economy will be less.

Such is the “second derivative” effect we explained previously.

“In calculus, the second derivative, or the second-order derivative, of a function (f) is the derivative of the derivative of (f.)” – Wikipedia

In English, the “second derivative” measures how the change rate of a quantity is itself changing.

I know, still confusing.

Let’s run an example:

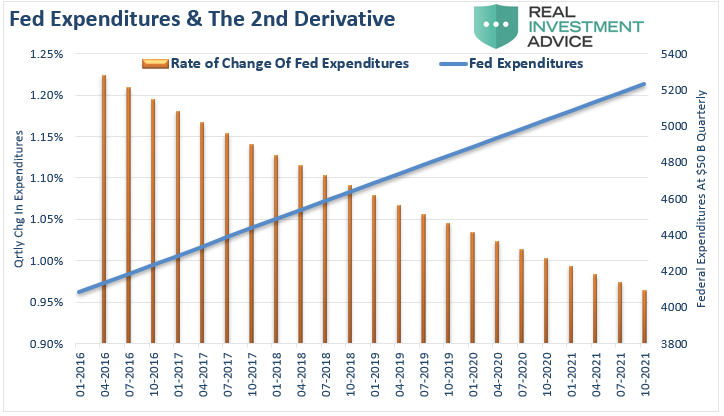

As Government spending grows sequentially larger, each additional round of expenditures will have less and less impact on the total. Going back to 2016, not including the CARES Act, the Government increased spending by roughly $50 billion each quarter on average. If we run a hypothetical model of Government expenditures at $50 billion per quarter, you can see the issue of the “second derivative.”

In this case, even though Federal expenditures are increasing at $50 Billion per quarter, the rate of change declines as the total spending increase.

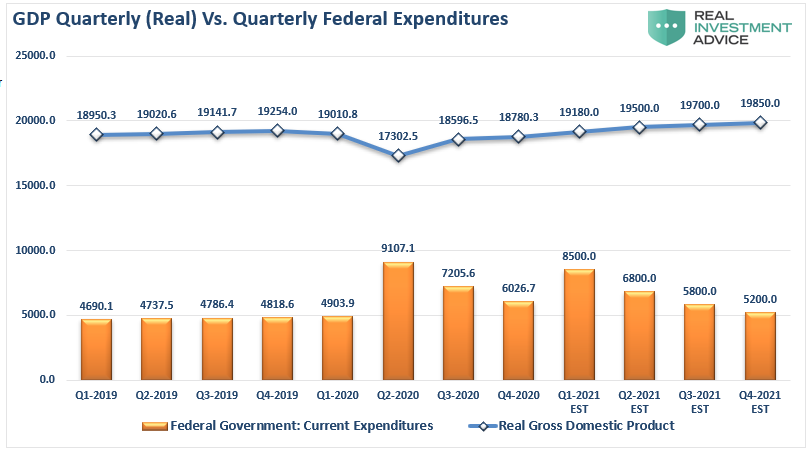

The following chart shows how the “second derivative” is already undermining both fiscal and monetary stimulus. Using actual data going back to Q1-2019, Federal Expenditures remained relatively stable through Q1-2020, along with real economic growth. However, in Q2-2020, with our estimates through 2021, Federal Expenditures will double. However, economic growth rates will slow quickly after the stimulus expires.

The chart below shows the inherent problem. While the additional fiscal stimulus may boost short-term economic growth, its impact becomes less over time.

However, this is ultimately the problem with all debt-supported fiscal and monetary programs.

As stated, even with the additional stimulus package, the outcome will be muted. If we assume our current estimates for GDP growth over the next 4-quarters, which align with mainstream consensus, growth will quickly fade back to long-term trends.

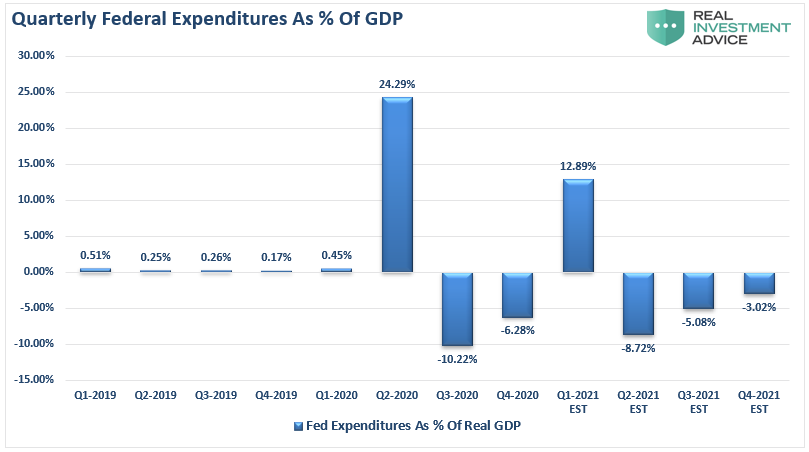

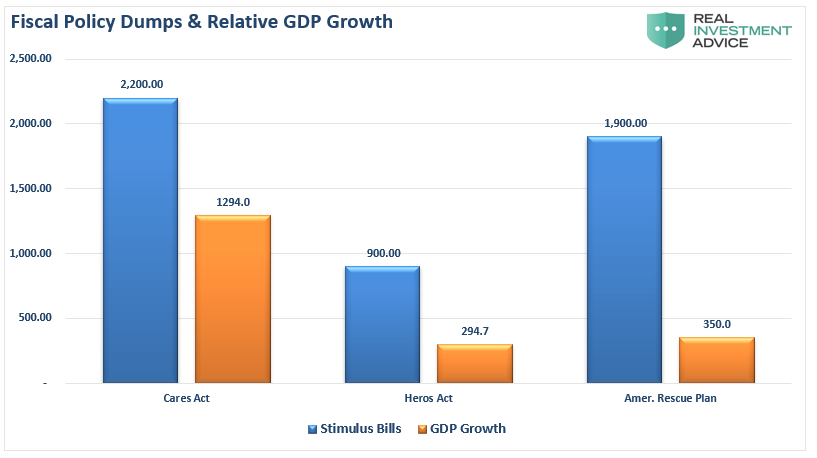

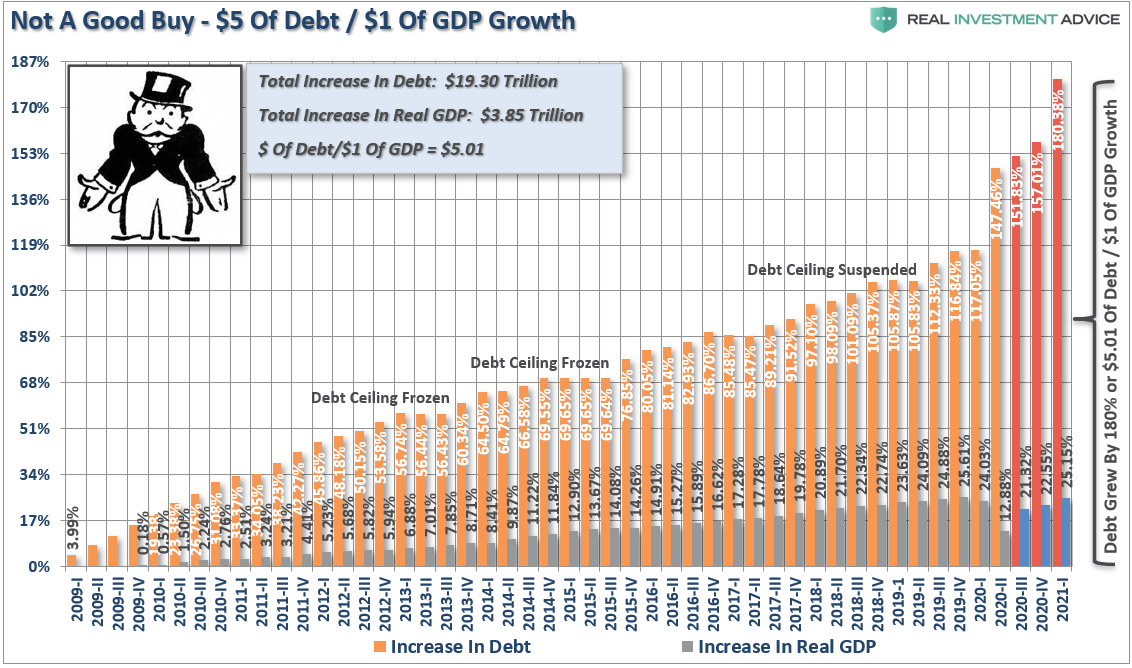

As noted above, it requires increasing levels of debt to generate lower rates of economic growth. The chart below shows the previous and estimated CARES Acts and their impact on GDP growth.

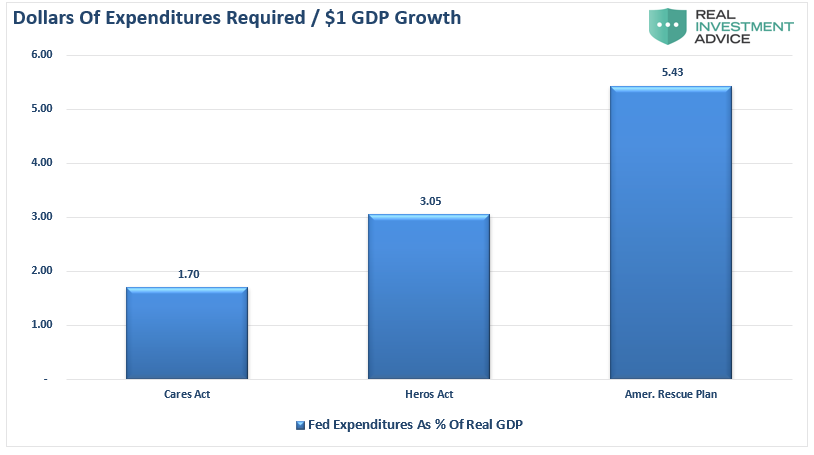

To understand this better, we can view it from how many dollars it requires to generate $1 of economic growth. Following the economic shutdown, when economic activity went to zero, each dollar of input had a more considerable impact as the economy restarted. However, going into 2021, economic activity has already recovered and started to stabilize at a slightly lower level than seen previously.

Given that stabilization of activity, it will require more dollars to generate economic growth in the future. As shown, it will need nearly $5.50 of debt-supported expenditures to create $1 of economic growth.

Here is the exciting part. That is NOT a new thing. As I discussed previously, “The One-Way Trip Of American Debt,” the economy requires $5.01 of debt to create $1 of growth. While not a great return on investment, it will worsen as debt continues to retard economic growth.

As Mr. Sparks states, more debt doesn’t lead to more robust economic growth rates or prosperity. Since 1980, the overall increase in debt has surged to levels that currently usurp the entirety of economic growth. With economic growth rates now at the lowest levels on record, the change in debt continues to divert more tax dollars away from productive investments into the service of debt and social welfare.

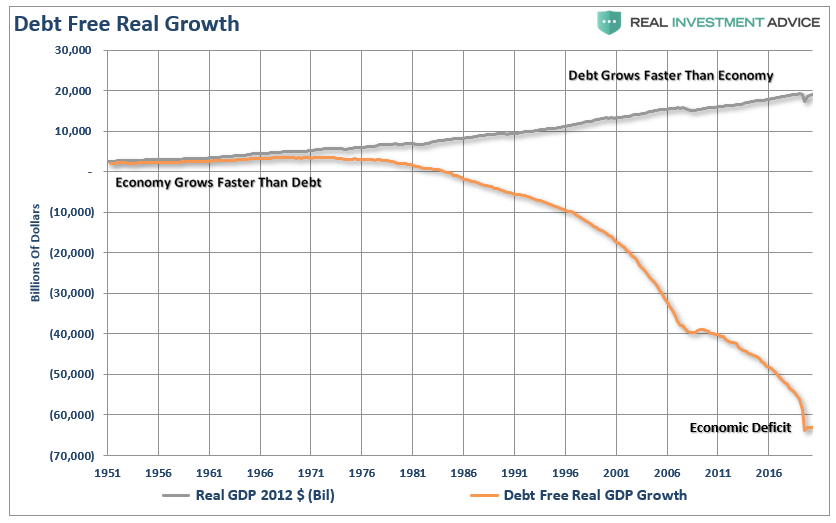

Another way to view the impact of debt on the economy is to look at what “debt-free” economic growth would be. In other words, without debt, there has been no organic economic growth.

The economic deficit has never been more significant. For the 30 years from 1952 to 1982, the economic surplus fostered a rising economic growth rate, which averaged roughly 8% during that period. Such is why the Federal Reserve has found itself in a “liquidity trap.”

Interest rates MUST remain low, and debt MUST grow faster than the economy, just to keep the economy from stalling out.

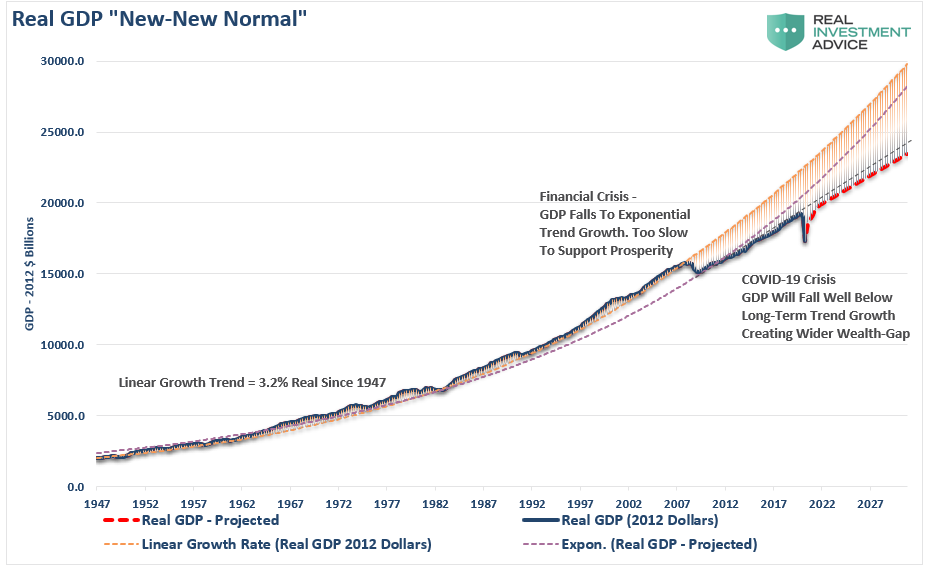

The deterioration of economic growth is seen more clearly in the chart below.

From 1947 to 2008, the U.S. economy had real, inflation-adjusted economic growth than had a linear growth trend of 3.2%.

However, following the 2008 recession, the growth rate dropped to the exponential growth trend of roughly 2.2%. Unfortunately, instead of reducing outstanding debt problems, the Federal Reserve provided policies that fostered even greater unproductive debt and leverage levels.

Following the 2020 recession, the economic growth trend will again decline below the previous growth trend. Even with our more optimistic assumptions about economic recovery, the trend of economic growth will weaken. Such is simply a function of the massive amounts of debt added to the overall system, which will retard future economic growth.

Our conclusions from the initial analysis remain the same:

“The ‘trap’ that lawmakers, along with the Fed, have now fallen into is that ‘stimulus’ only pulls forward ‘future consumption.’ As we saw after the initial CARES act, as soon as financial supports evaporated, so did economic growth.

The hope over the last decade was the economy would eventually “catch fire” grow organically. Such would allow Central Banks to reverse monetary supports. However, such has never occurred. Each time Central Banks reduce monetary supports, the economy stalls or worse.

It is likely that “something has gone wrong” for the Federal Reserve. The ability to pull-forward future consumption through monetary interventions has been reached. Despite ongoing hopes of ‘higher growth rates’ in the future, such will likely not be the case until the debt overhang gets cleared.”

While the U.S. economy will indeed exit the recession in 2021, it may be a statistical result rather than an economic recovery leading to broader prosperity.

The most significant risk of the latest stimulus package is a surge in inflationary pressures, which undermines the stimulus’s benefit. That concern will manifest itself as a stagflationary environment where wages remain suppressed while costs of living rise.

Due to the debt, demographics, and monetary and fiscal policy failures, the long-term economic growth rate will run well below long-term trends. Such will only continue to widen the wealth gap, increase welfare dependency, and socialism continuing to usurp the “golden goose” of capitalism.

The post #MacroView: Debt Fueled Spending Won’t Create Growth appeared first on RIA.

Fed Emergency Bank Bailout Facility Usage Hits New Record High; Money Market Funds See Small…

US Homeowner Equity Drops For First Time Since 2012 The housing bull market has peaked…

JPMorgan and Citigroup Are Using the Same Accounting Maneuver as Silicon Valley Bank on Hundreds…

At Year End, 4,127 U.S. Banks Held $7.7 Trillion in Uninsured Deposits; JPMorgan Chase, BofA,…

Do you really own something if someone forces you to make never-ending (and ever-increasing) payments…

Doug Casey On Why The US Is Headed Into Its 'Fourth Turning' Authored by Doug…

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}