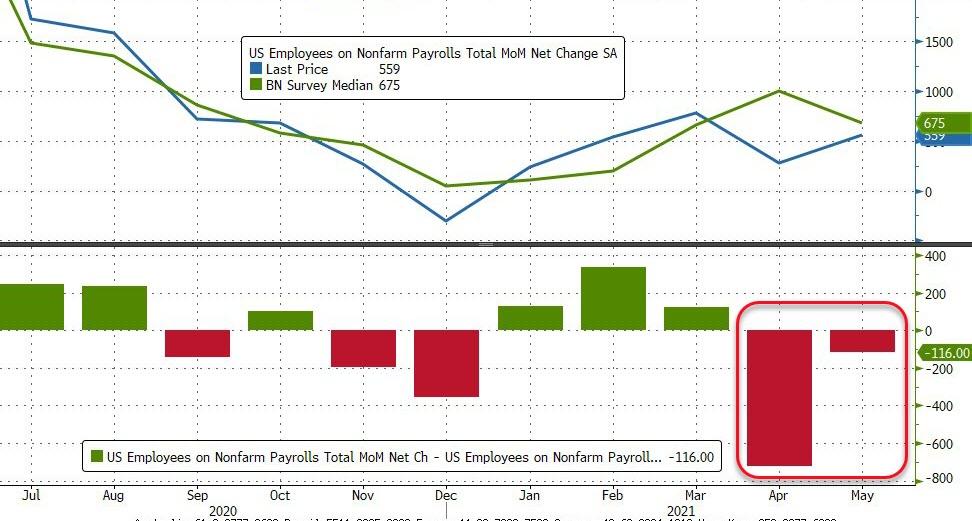

May Payrolls Miss: 559K Jobs Added, Below Expectations; Unemployment Rate Drops

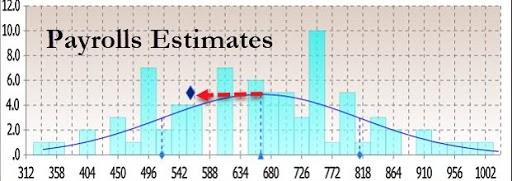

With so much of the recent labor market discourse focusing on widespread shortages resulting from Uncle Sam’s generous unemployment benefits (15 million people still collecting some form of weekly unemployment benefit), today’s jobs report which is expected to show a substantial rebound from April’s big miss, was set to be defining: another big miss and the shortage narrative would dominate for a long time, a big beat would meanwhile spark renewed reflation worries.

Well, it appears that "shortages" won out in the end because moments ago the BLS reported that in April just 559K jobs were added, which while a big improvement to April’s upward revised 278K…

… was another big miss compared to the 675K expectations.

While the miss was material, it was within the range of expectations, less than 1 SD compared to consensus, and far less pronounced than last month’s miss.

The change in total nonfarm payroll employment for March was revised up by 15,000, from +770,000 to +785,000, and the change for April was revised up by 12,000, from +266,000 to +278,000. With these revisions, employment in March and April combined was a modest 27,000 higher than previously reported.

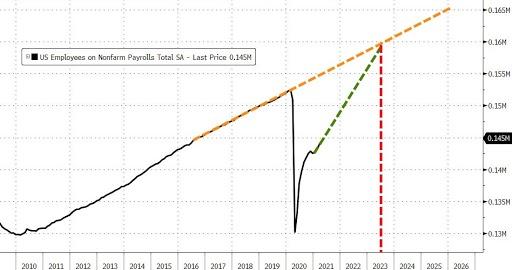

Nonfarm payroll employment is now down by 7.6 million, or 5.0%, from its pre-pandemic level in February 2020. Notable job gains occurred in leisure and hospitality, in public and private education, and in health care and social assistance in May.

The offset to the headline miss is that the unemployment rate dropped from 6.1% to 5.8%, coming below expectations of 5.9%, and reversing last month’s modest increase.

Yet digging into the numbers reveals another potential problem: the reason why the unemployment rate fell is that 160,000 people left the labor force in May. That’s not what you’d like to see in an economic recovery. Ideally, you see businesses reopening, encouraging people to start looking for work again.

Among the major worker groups, the unemployment rates declined in May for teenagers (9.6 percent), Whites (5.1 percent), and Hispanics (7.3 percent). The jobless rates for adult men (5.9 percent), adult women (5.4 percent), Blacks (9.1 percent), and Asians (5.5

percent) showed little change in May.

Among the unemployed, the number of persons on temporary layoff declined by 291,000 to 1.8 million in May. This measure is down considerably from the recent high of 18.0 million in April 2020 but is 1.1 million higher than in February 2020. The number of permanent job losers decreased by 295,000 to 3.2 million in May but is 1.9 million higher than in February 2020.

The labor force participation rate also dropped to 61.6% in May from 61.8%, having remained within a narrow range of 61.4 percent to 61.7 percent since June 2020. The participation rate is 1.7% points lower than in February 2020. The employment-population ratio, at 58.0 percent, was also little changed in May but is up by 0.6 percentage point since December 2020. However, this measure is 3.1 percentage points below its February 2020 level.

The number of persons not in the labor force who currently want a job was essentially unchanged over the month at 6.6 million but is up by 1.6 million since February 2020. These individuals were not counted as unemployed because they were not actively looking for work during the last 4 weeks or were unavailable to take a job.

Among those not in the labor force who currently want a job, the number of persons marginally attached to the labor force, at 2.0 million, changed little in May but is up by 518,000 since February 2020. These individuals wanted and were available for work and had looked for a job sometime in the prior 12 months but had not looked for work in the 4 weeks preceding the survey. The number of discouraged workers, a subset of the marginally attached who believed that no jobs were available for them, was 600,000 in May, little changed from the previous month but 199,000 higher than in February 2020.

And another notable fact: in May, 7.9 million persons reported that they had been unable to work because their employer closed or lost business due to the pandemic.

The number of persons jobless less than 5 weeks declined by 391,000 to 2.0 million. The number of long-term unemployed (those jobless for 27 weeks or more) declined by 431,000 to 3.8 million in May but is 2.6 million higher than in February 2020. These long-term unemployed accounted for 40.9 percent of the total unemployed in May.

There was more good news on the wage front, where average hourly earnings rose from 0.4% to 2.0%, beating expectations of 1.6%.

Average hourly earnings for all employees on private nonfarm payrolls increased by 15 cents to $30.33 in May, following an increase of 21 cents in April. Average hourly earnings of private-sector production and nonsupervisory employees rose by 14 cents to $25.60 in May, following an increase of 19 cents in April. The data for the last 2 months suggest that the rising demand for labor associated with the recovery from the pandemic may have put upward pressure on wages. However, because average hourly earnings vary widely across industries, the large employment fluctuations since February 2020 complicate the analysis of recent trends in average hourly earnings.

In May, the average workweek for all employees on private nonfarm payrolls was 34.9 hours for the third month in a row. In manufacturing, the average workweek rose by 0.1 hour to 40.5 hours, and overtime increased by 0.1 hour to 3.3 hours. The average workweek for production and nonsupervisory employees on private nonfarm payrolls declined by 0.1 hour to 34.3 hours.

A breakdown of jobs by sector:

Bottom line: a stronger jobs report, but still far below where it needs to be for the Fed to concede that the labor market is normalizing. And, of course, the paradox is that this is mostly due to the government’s generous handouts as CIBC economist Katherine Judge wrote:

“Our research suggests that generous unemployment benefit supplements have been the main factor holding employment gains back amidst record levels of job openings, but with many states moving to end the supplements in June, we expect millions of jobs to be added over the summer months.”

Still, Judge said she expects that a pick-up in job growth over the summer should be “enough to allow the Fed to announce at its September meeting a tapering of QE to start in early 2022.”

FX strategist Viraj Patel was not so sure: commenting on the jobs report, he said that the "modest NFP gains of +559k will be a disappointment for Fed hawkish expectations. $USD weaker across the board as US rates drop. Likely that the wage inflation will be ignored due to distortions but a mixed bag overall with participation rate lower. Only +ve is U-6 rate down."

Bloomberg’s Chris Antsey agrees with this skeptical view, saying that the Fed’s leadership "is likely to see this report as a modest improvement but not near the “substantial further progress” on employment required to taper its bond-buying program. While inflation is now topping the central bank’s 2% goal, jobs remain not really close to the goal."

Finally, the political blowback will be big: as Bloomberg notes, Republican lawmakers will immediately "hit the Biden administration for the extension of the supplemental $300-a-week unemployment benefits included in the $1.9 trillion pandemic-relief bill", which they correctly argue that’s what’s stopping some people from taking jobs; people can earn more or at least as much just sitting at home and collecting benefits. Expect Biden to rebut that argument when he speaks about these numbers later this morning.

Tyler Durden

Fri, 06/04/2021 – 08:34

Fed Emergency Bank Bailout Facility Usage Hits New Record High; Money Market Funds See Small…

US Homeowner Equity Drops For First Time Since 2012 The housing bull market has peaked…

JPMorgan and Citigroup Are Using the Same Accounting Maneuver as Silicon Valley Bank on Hundreds…

At Year End, 4,127 U.S. Banks Held $7.7 Trillion in Uninsured Deposits; JPMorgan Chase, BofA,…

Do you really own something if someone forces you to make never-ending (and ever-increasing) payments…

Doug Casey On Why The US Is Headed Into Its 'Fourth Turning' Authored by Doug…

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}