Since the “Financial Crisis,” the hope was that inflating asset prices would trickle down into economic growth. Unfortunately, after a decade of monetary interventions and artificially suppressed interest rates, the wealth gap has exploded. More problematic is the Fed has forced investors to take on excess risk due to the lack of alternatives.

I previously wrote an article on retirees’ primary problem: the 4% Rule is dead. To wit:

“The 4% Rule has long been used as a guideline for retirees in determining how much they should be able to withdraw from their retirement account while still maintaining a balance that will allow for the same income stream to flow through their golden years.”

The 4% rule originally suggested that once retired; portfolio allocations shift to ultra-safe Treasury bonds. Such an allocation shift provides for the income required to live on, plus a guarantee of the principal.

Here’s the problem.

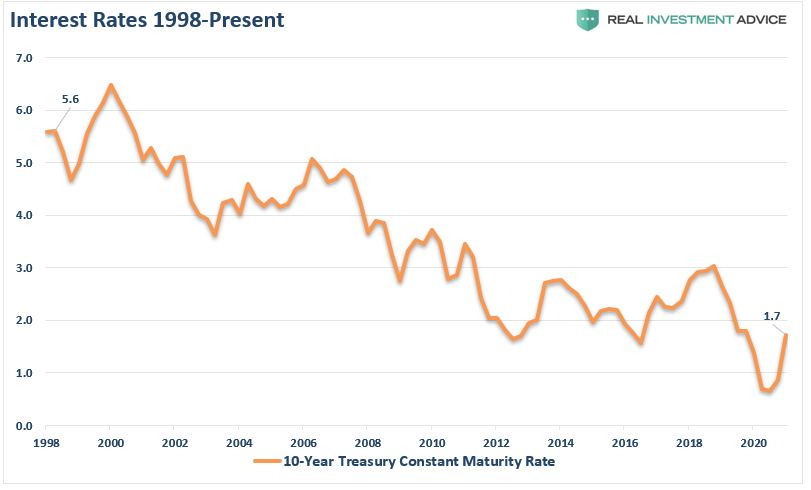

When the 4% rule originated, Treasury yields were 5%. Today, they are just slightly above historic lows set during 2020.

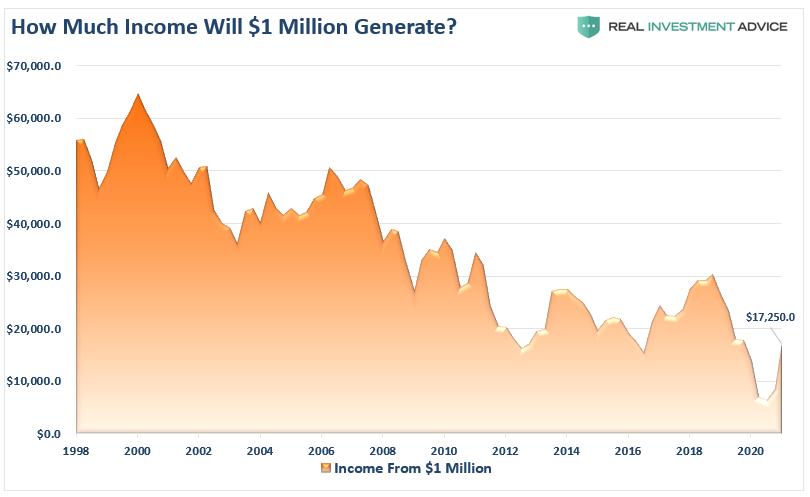

Such is a massive problem for retirees today. As shown, $1 million will no longer generate a $50,000 income for retirement. Today, it is just $17,250/year, much better than the paltry $5500 set at the lows in 2020.

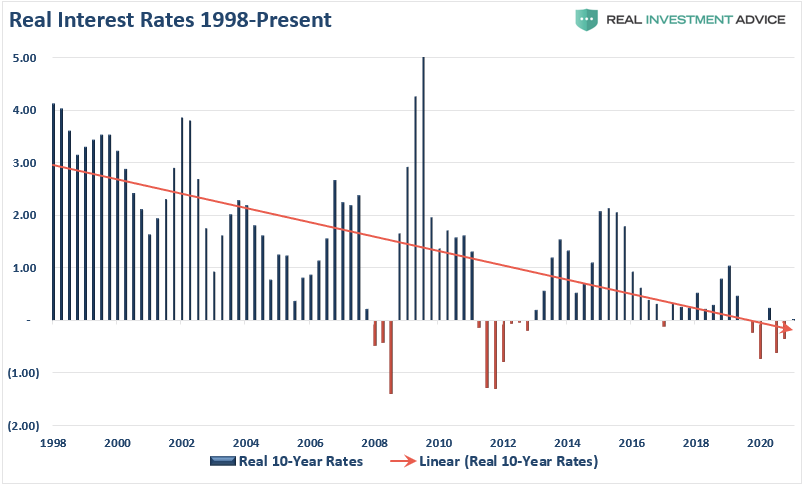

However, that is a deceptive number due to the lack of an inflation adjustment. When we look at “real rates,” the problem for savers because more apparent.

With “real” rates currently negative, what are “savers” supposed to do?

The question we should be asking is, how did we get here?

For that answer, we have to go back to 1982 as President Reagan launched a mission to break the back of spiraling inflation and interest rates. At the same time, he was working to restart the U.S. economy following two back-to-back recessions.

For this task, he joined forces with then-Fed Chairman Paul Volker to start using active monetary policy to fight inflation and create employment. Reagan engaged in deficit spending to fill gaps in the economy, cut taxes, and deregulated the banking system. It worked, he produced more than 9-million jobs, and inflation and interest rates started falling, leading to a pickup in economic growth rates.

What he didn’t realize then was that he had just opened “Pandora’s box.”

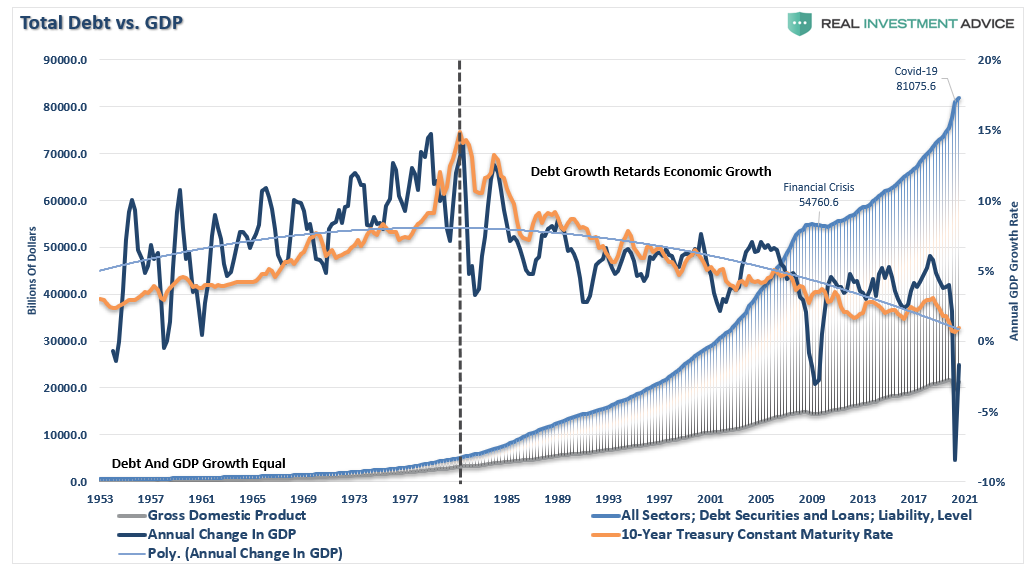

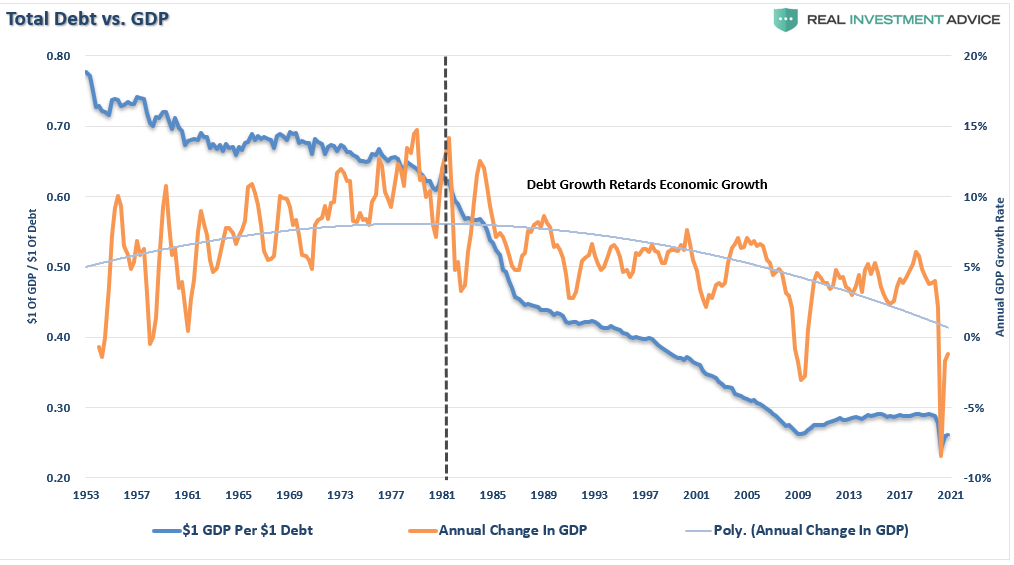

Since 1980, the overall increase in debt has surged to levels that currently usurp the entirety of economic growth. With economic growth rates now at the lowest levels on record, the change in debt continues to divert more tax dollars away from productive investments into the service of debt and social welfare.

We can view the impact of debt on the economy by analyzing the economic growth created. As shown, it takes an increasing amount of debt to generate each dollar of economic growth.

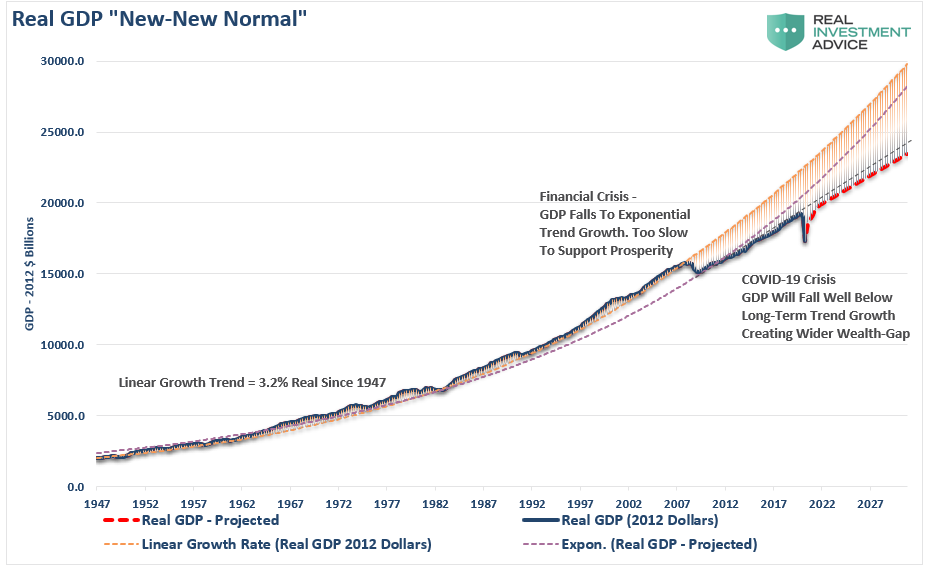

The deterioration of economic growth is seen more clearly in the chart below.

From 1947 to 2008, the U.S. economy had real, inflation-adjusted economic growth than had a linear growth trend of 3.2%.

However, following the 2008 recession, the growth rate dropped to the exponential growth trend of roughly 2.2%. Unfortunately, instead of reducing outstanding debt problems, the Federal Reserve engaged in policies that expanded unproductive debt and leverage.

Coming out of the 2020 recession, the economic trend of growth will be somewhere between 1.5% and 1.75%. Given the amount of debt added to the overall system due to the pandemic, the ongoing debt service will continue to retard economic growth.

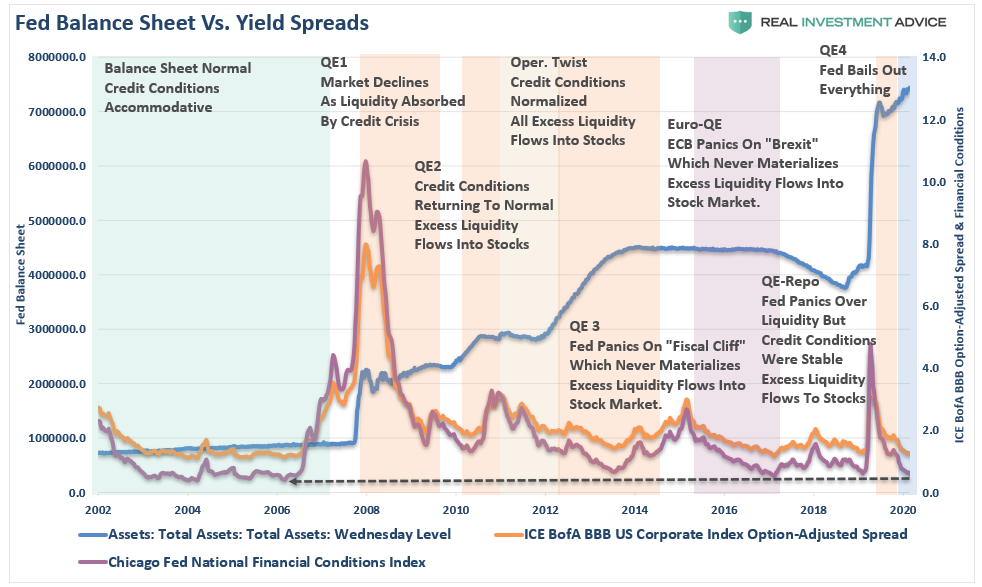

The “debt problem” is also why the Federal Reserve has found itself in a “liquidity trap.”

Interest rates MUST remain low, and debt MUST grow faster than the economy, just to keep the economy from stalling out.

Before you argue that point, ask yourself this one question:

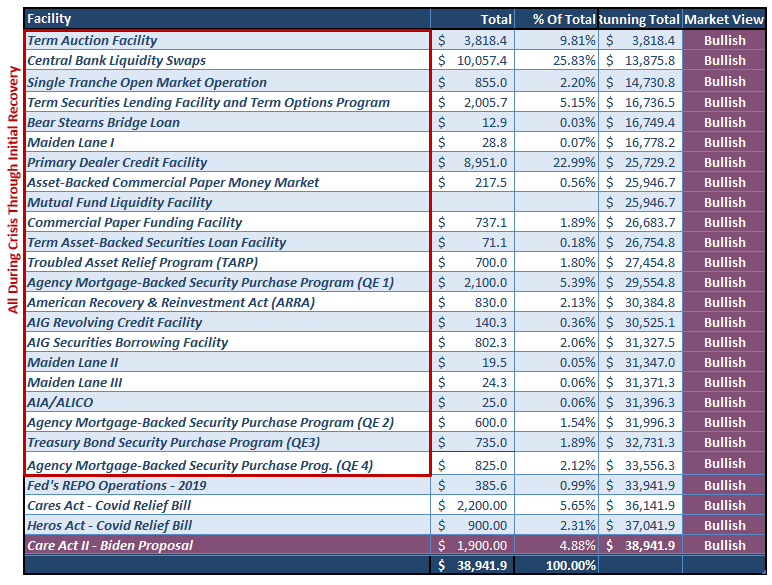

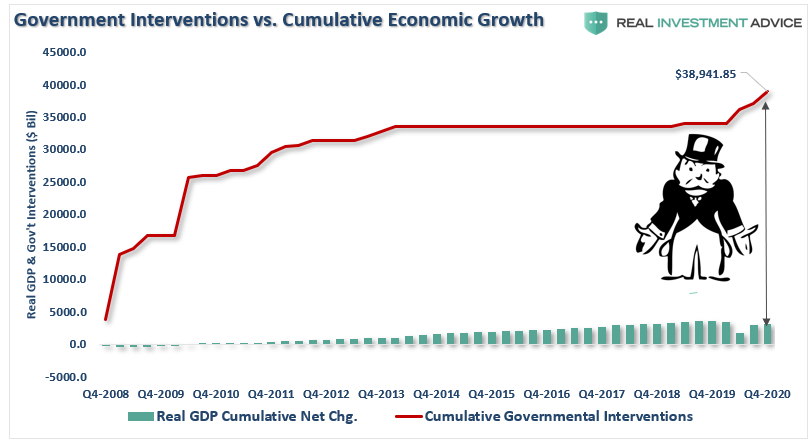

If the economy was strong, employment was full, and financial prosperity was high, then why did it require almost $39 trillion since 2009 to keep a $20 trillion economy afloat?

However, the following chart more clearly shows the amount of support required over the last decade to keep the economy from faltering.

Given the economy is driven by “consumption,” the Fed believed that promoting “asset inflation” would lead to increased “confidence,” thereby creating economic growth. Such was the exact point made in 2010 by Ben Bernanke,

“This approach eased financial conditions in the past and, so far, looks to be effective again. Stock prices rose and long-term interest rates fell when investors began to anticipate the most recent action. Easier financial conditions will promote economic growth. For example, lower mortgage rates will make housing more affordable and allow more homeowners to refinance. Lower corporate bond rates will encourage investment. And higher stock prices will boost consumer wealth and help increase confidence, which can also spur spending.”

Bernanke, then Yellen, and Jerome Powell failed to grasp that the “trickle-down effect” never trickled down. While consumers piled on more debt to make ends meet, those in the top-10% with money to invest got substantially wealthier.

For investors who have money invested in the financial markets, the Fed’s actions have had one very predictable outcome. By keeping interest rates pegged at zero for nearly a decade, the Fed forced “savers” to take on more “risk” for even a marginal rate of return to pace inflation.

A recent article by The American Insitute noted this point:

“In fact, risk tolerances are up across the board. There are anecdotes, of course, but the evidence is clear in trends of some of the most historically risky markets. The stock market, once a fairly mid-range option for risk and return, has gone from a complement to a substitute for the role that bank accounts or Treasury bonds once filled.“

For example, investors are now taking on far more risk in “credit” than they get compensated for. Such has been the legacy of the Federal Reserve interventions since the turn of the century.

Given a decade of monetary interventions, investors have come to believe that “risk” has been permanently mitigated by the Federal Reserve. For that reason, investors have piled into “credit risk” and “equity risk” to an extreme degree.

Such is entirely understandable when money market yields, bond yields, and equity yields are nearly their lowest in history.

Investors seemingly don’t have any choice.

Investors are currently playing a “Lose-Lose” game.

Such was the conclusion from the American Institute:

“The Federal Reserve has done more in the past 25 years than its founding legislators and early governors surely ever conceived it would. With that in mind, one wonders what the end game is, especially in light of two facts.

- First, that the inclination of monetary authorities the world over is toward lower and lower thresholds for intervention.

- And second, that fiscal and monetary policies have a way of suddenly finding limits when the tax-paying everyman is on the receiving end.

If there is a component of the growing disposition for risk inspired by the idea that the Fed will swoop in to save retail investors from failed ETFs, collapsed SPAC prices, a wave of microcap stock delistings, or any other consequence of their understandable but reluctant march up the risk curve, it is ill-advised. Any lasting solution is far more likely to come from markets themselves.”

So what do you do?

The analysis above reveals the important points individuals should consider in their financial planning process:

No matter what age you are, investing for retirement is a conservative and careful process designed to outpace inflation over time. Such doesn’t mean you should never invest in the stock market; it just means that you should construct the portfolio to deliver a rate of return sufficient to meet your long-term goals with minimal risk.

Most likely, whatever retirement planning you have done is overly optimistic.

Change your assumptions, ask questions, and plan for the worst.

Importantly, understand how much “risk” you are taking to make returns. Taking on “risk” during rising markets is one thing, but it can be devastating during declines.

The Fed hasn’t given you many choices, but sometimes “no return” is better than the alternative.

The post The Fed Has Forced Investors To Take On Excess Risk appeared first on RIA.

RIA details the complicated environment investors face over the next few decades as decent returns may be harder to come by thanks to the Fed. One risk I believe they fail to mention is government control of retirement accounts.

I’m hesitant to mention this opinion because 99.99% of people will not take this seriously and it damages any credibility I may or may not have.

Before you dismiss this idea as doomsday, I recommend you sign up

Fed Emergency Bank Bailout Facility Usage Hits New Record High; Money Market Funds See Small…

US Homeowner Equity Drops For First Time Since 2012 The housing bull market has peaked…

JPMorgan and Citigroup Are Using the Same Accounting Maneuver as Silicon Valley Bank on Hundreds…

At Year End, 4,127 U.S. Banks Held $7.7 Trillion in Uninsured Deposits; JPMorgan Chase, BofA,…

Do you really own something if someone forces you to make never-ending (and ever-increasing) payments…

Doug Casey On Why The US Is Headed Into Its 'Fourth Turning' Authored by Doug…

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}