March 2, 2021 | Ben Hunt | 6 Comments | Note33+

The Opposite of 2008

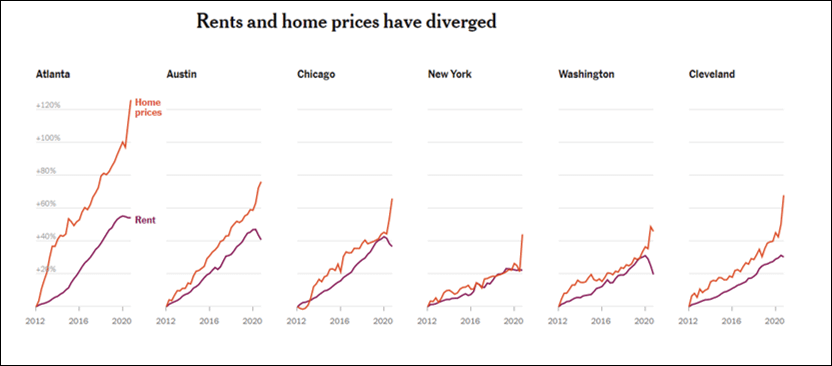

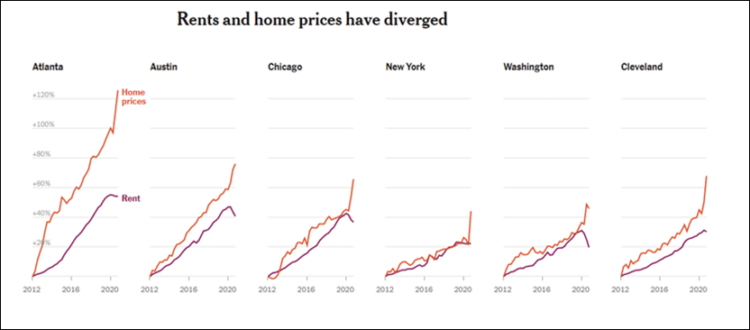

In late 2007 I started counting the For Sale signs on the 20 minute drive to work through the neighborhoods of Weston and Westport, CT. I’m not exactly sure why it made my risk antenna start quivering in the first place … honestly, I just like to count things – anything – when I’m doing a repetitive task. Coming into 2008 there were a mid-teen number of For Sale signs on my regular route, up from high single-digits in 2007. By May of 2008 there were 35+ For Sale signs.If there’s a better real-world signal of financial system distress than everyone who takes Metro North from Westport to Grand Central trying to sell their homes all at the same time and finding no buyers … I don’t know what that signal is. The insane amount of housing supply in Wall Street bedroom communities in early 2008 was a crucial datapoint in my figuring out the systemic risks and market ramifications of the Great Financial Crisis.Last week, for the first time in years, I made the old drive to count the number of For Sale signs. Know how many there were?Zero.And then on Friday I saw this article from the NY Times – Where Have All the Houses Gone? – with these two graphics:

I mean … my god.Here’s where I am right now as I try to piece together what the Opposite of 2008 means for markets and real-world.1) Home price appreciation will not show up in official inflation stats. In fact, given that a) rents are flat to declining, and b) the Fed uses “rent equivalents” as their modeled proxy for housing inputs to cost of living calculations, it’s entirely possible that soaring home prices will end up being a negative contribution to official inflation statistics. This is, of course, absolutely insane, but it’s why we will continue to hear Jay Powell talk about “transitory” inflation that the Fed “just doesn’t see”.2) Cash-out mortgage refis and HELOCs are going to explode. On Friday, I saw that Rocket Mortgage reported on their quarterly call that refi applications were coming in at their fastest rate ever. As the kids would say, I’m old enough to remember the tailwind that home equity withdrawals provided for … everything … in 2005-2007. This will also “surprise” the Fed.3) Middle class (ie, home-owning) blue collar labor mobility is dead. If you need to move to find a new job, you’re a renter. You’re not going to be able to buy a home in your new metro area. That really doesn’t matter for white collar labor mobility, because you can work remotely. You don’t have to move to find a new job if you’re a white collar worker. Or if you want to put this in terms of demographics rather than class, this is great for boomers and awful for millennials and Gen Z’ers who want to buy a house and start a family.4) As for markets … I think it is impossible for the Fed NOT to fall way behind the curve here. I think it is impossible for the Fed NOT to be caught flat-footed here. I think it is impossible for the Fed NOT to underreact for months and then find themselves in a position where they must overreact just to avoid a serious melt-up in real-world prices and pockets of market-world. Could a Covid variant surge tap the deflationary brakes on all this? Absolutely. But let’s hope that doesn’t happen! And even if it does happen, that’s only going to constrict housing supply still more, which is the real driver of these inflationary pressures.Bottom line …I am increasingly thinking that both a Covid-recovery world AND a perma-Covid world are inflationary worlds, the former from a demand shock and the latter from a supply shock to the biggest and most important single asset market in the world – the US housing market.It’s just like 2008, except … the opposite.