“Willfully Blind” Bulls Run As Liquidity Floods Market

Authored by Lance Roberts via RealInvestmentAdvice.com,

As liquidity floods the market, the bulls continue to run the market. However, was the recent consolidation enough to reset market exuberance?

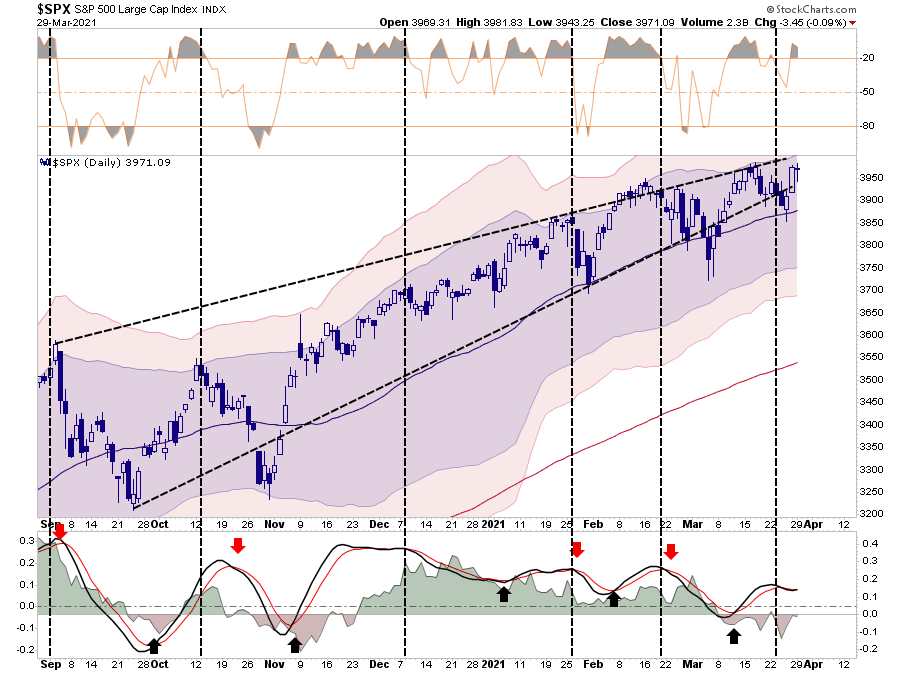

Over the last few weeks, I discussed the weekly “sell signals.” Such suggested upside would be somewhat limited for markets near-term. However, that flood of liquidity also limited the downside. Such has indeed been the case, as volatile markets made little headway since February, but dips continue to get bought.

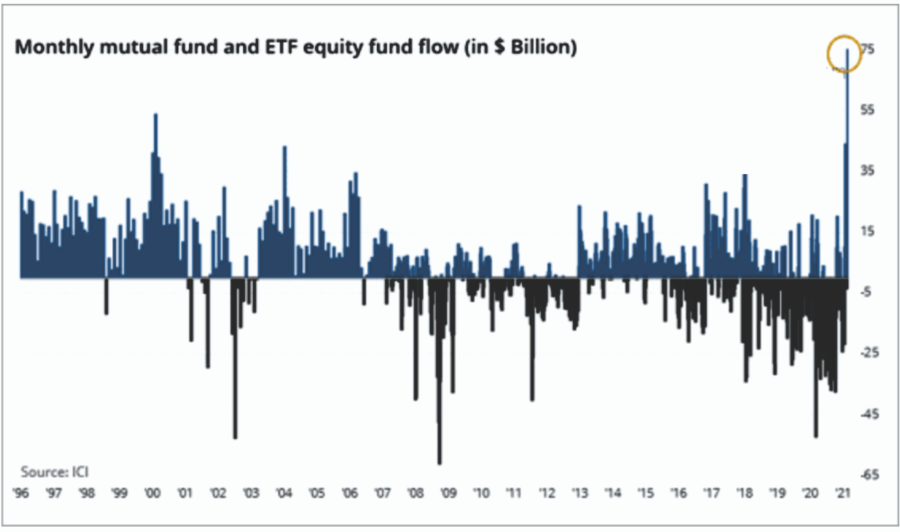

With “stimmy” checks hitting bank accounts, “retail trading” stocks should get a boost as former gamblers and “pandemic lock-ins” return to Robinhood.

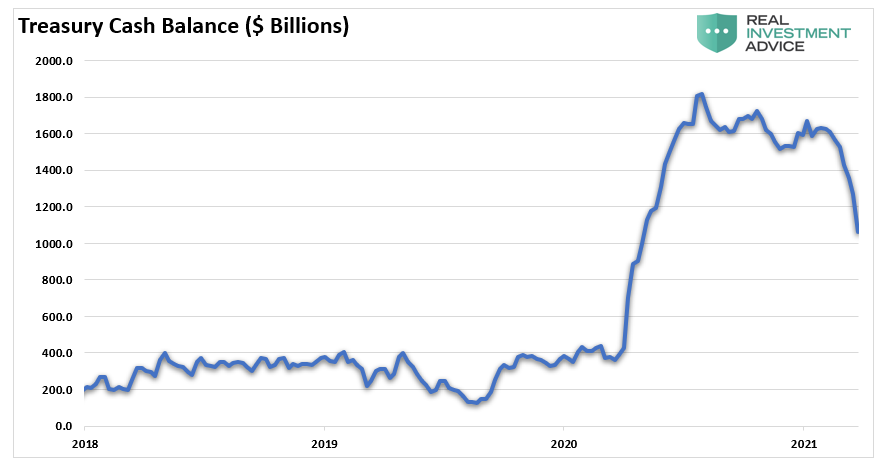

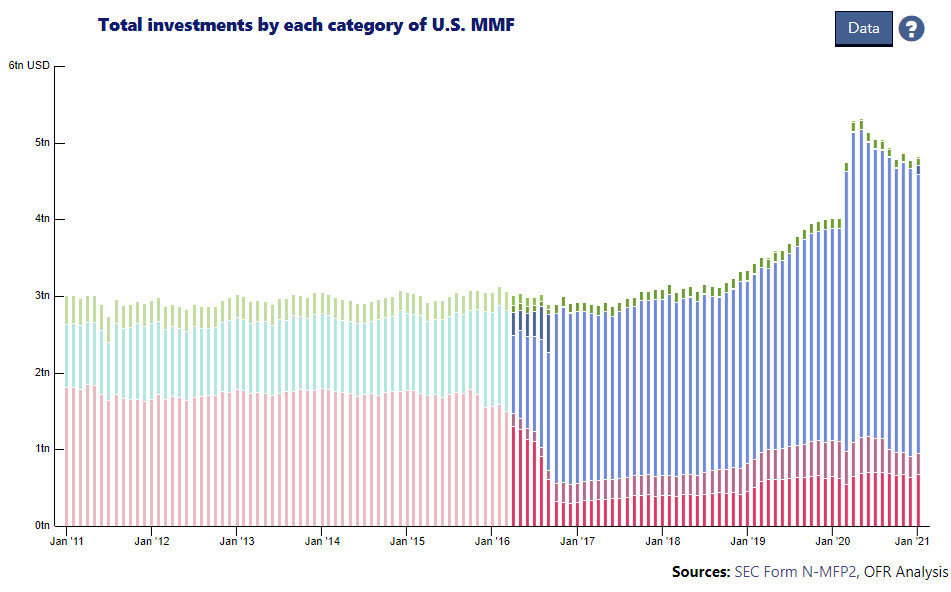

Furthermore, the surge in liquidity from the CARES Act last March is now working its way back into the economy as well. Those Treasury balances are getting drawn down to fund expenditures such as extended unemployment benefits.

Unsurprisingly, all this liquidity is finding its way into the markets.

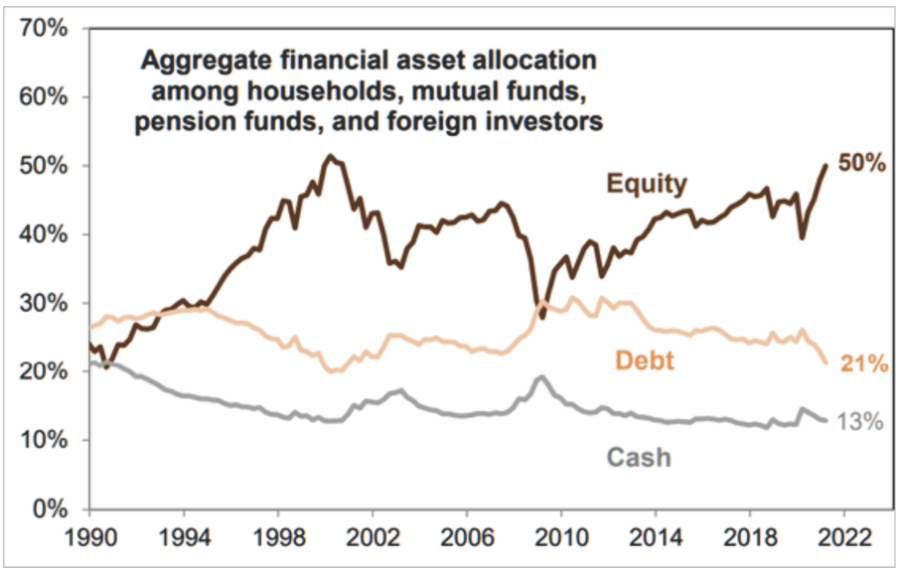

Such has pushed equity allocations to nearly “Dot.com” level highs.

In other words, the bulls see “no risk” in being invested in “risk” assets.

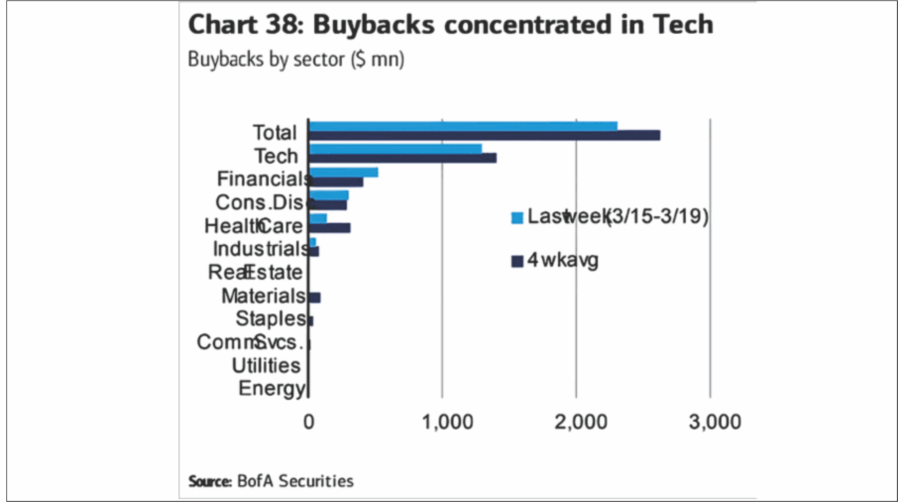

As I noted in “Powell’s Easy Money Promise,” stock buybacks have returned with a vengeance.

“No, this is not the ‘cash on the sidelines’ argument which I debunked previously. Following the pandemic, corporations drew down credit lines and hoarded cash due to economic uncertainty. Now, with expectations of recovery, corporations are once again beginning to deploy that cash.”

As I said then, while the mainstream media hope is all this cash will be flowing back into the economy, the reality is that it will primarily go to stock buybacks. Again, while not necessarily bad, it is the “least best” use of the company’s cash. Instead of expanding production, increasing sales, acquiring competitors, or making capital investments, the money gets used for a one-time boost to earnings on a per-share basis.

This past week, share buybacks hit a new record.

Not surprisingly, the most prominent players in buybacks are the ones that need to subsidize their earnings the most to beat estimates; technology and financials.

While share buybacks primarily are for the benefit of corporate insiders “cashing out,” it does have the effect of supporting asset prices as well. As I discussed in 2019, when stocks were hitting records amid record share repurchases:

“What is clear, is that the misuse, and abuse, of share buybacks to manipulate earnings and reward insiders has become problematic. As John Authers recently pointed out:

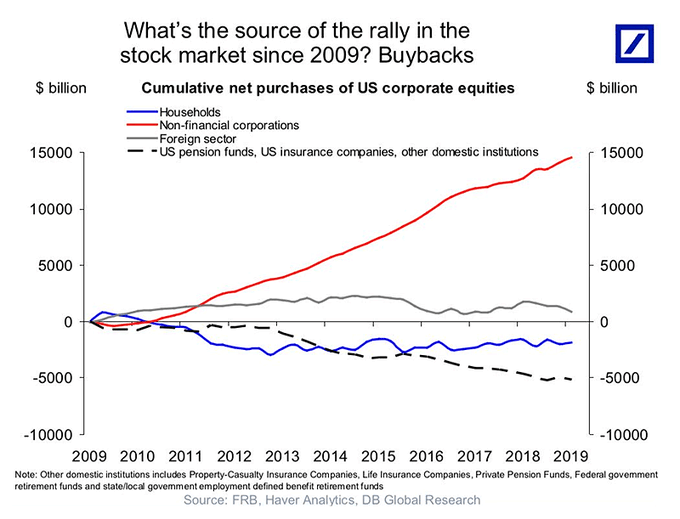

‘For much of the last decade, companies buying their own shares have accounted for all net purchases. The total amount of stock bought back by companies since the 2008 crisis even exceeds the Federal Reserve’s spending on buying bonds over the same period as part of quantitative easing. Both pushed up asset prices.’

In other words, between the Federal Reserve injecting a massive amount of liquidity into the financial markets, and corporations buying back their own shares, there have been effectively no other real buyers in the market.”

I bring this up for two reasons:

While Janet Yellen is okay with the buybacks, as she thinks the banks are healthier now, why doesn’t anyone ask the question:

“If banks are so healthy, why do they need a constant monetary stimulus to remain in business and a bailout every time the economy declines?”

It doesn’t sound very healthy to me. But for now, there is only one headline that matters:

The problem of assuming there is “no risk” is that it leads to “investor complacency.” As discussed in “Willful Blindness:”

“Willful blindness, also known as willful ignorance or contrived ignorance, is a term used in law. Being ‘willfully blind’ describes a situation where a person seeks to avoid civil or criminal liability for a wrongful act by keeping themselves unaware of the facts that would render them liable or implicated.

The phrase ‘willful blindness’ also means any situation in which people avoid facts to absolve themselves of their liability.

‘Investors regularly dismiss the ‘facts’ which run contrary to their current opinion. In behavioral investing terms this is ‘confirmation bias.’

As markets rise, investors take on exceedingly more risk with the full knowledge that such actions will have a negative consequence. However, that ‘negative consequence’ is dismissed by the ‘fear of missing out,’ or rather F.O.M.O.

As ‘greed’ overtakes ‘fear,’ investors become emboldened as rising markets reinforce their convictions. When the negative consequence occurs, instead of taking responsibility, they blame the media, Wall Street, or their advisor.”

This currently where we are in the markets today.

As discussed, with investors fully allocated, the risk remains that markets are trading at near-record extensions of longer-term means. The monthly chart below shows the current deviation from the long-term mean. Two things to note:

It is generally near market peaks when investors are the most complacent about risk. While I certainly agree in the shorter-term, the liquidity flood has mitigated downside risk; it only exacerbates longer-term consequences.

Currently, investors are very exuberant about markets, although they can get more so.

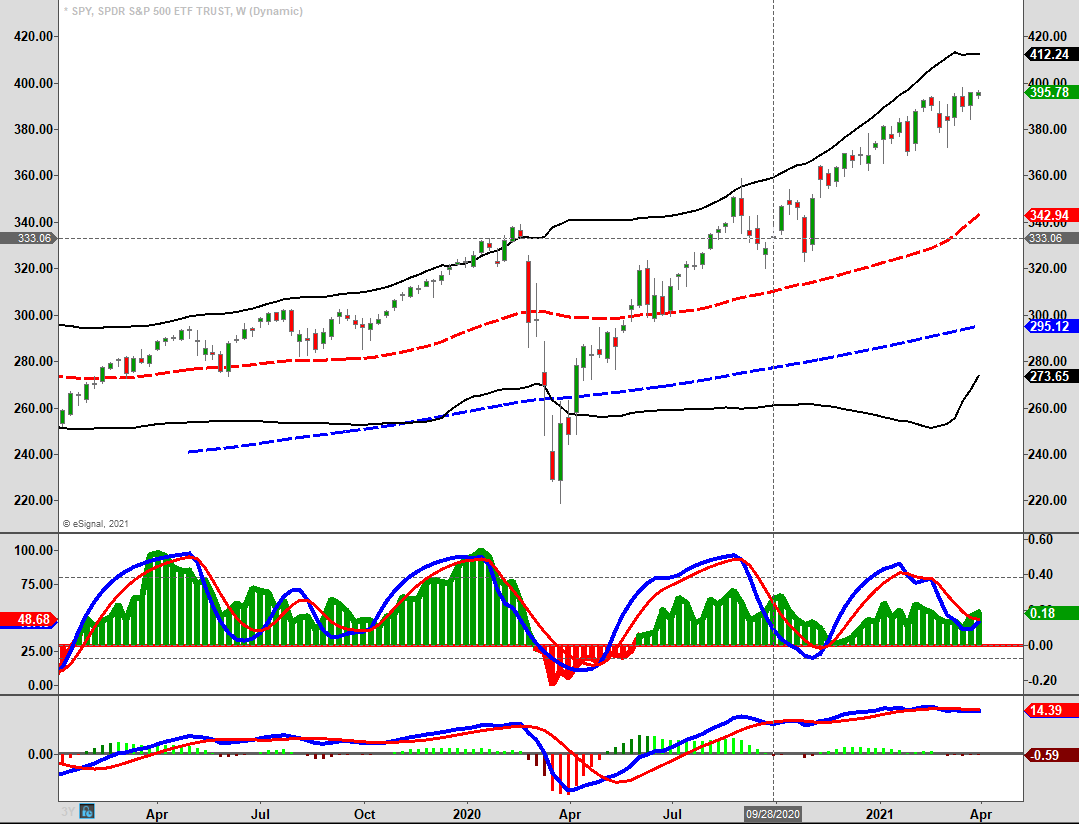

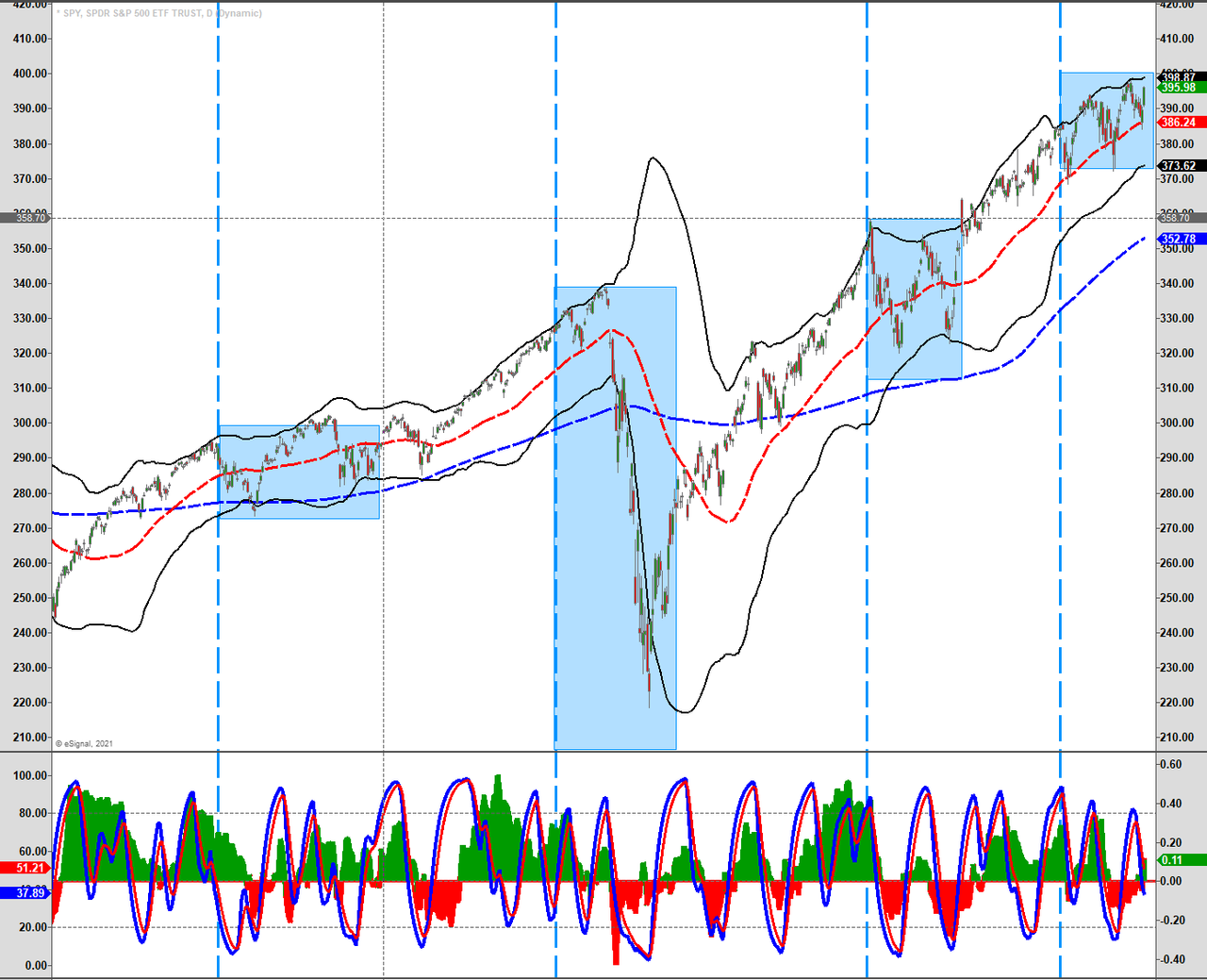

With the flood of stimulus into the market, another surge higher would not be a surprise. Such would correspond both with the peak of liquidity inflows and the peak in earnings and economic growth expectations. From a technical perspective, this also aligns with the weekly “money flow” index, turning positive. Typically, these weekly “buy” signals last roughly two to three months before reversing.

Note the blue vertical dashed lines below. Those lines are the weekly “buy” and “sell” signals overlaid on the daily chart. The blue boxes show where the daily and weekly sell signals converged previously.

When both indicators align on “sell signals,” blue boxes, market volatility rises markedly. However, markets tend to increase when both indicators align with “buy signals.”

With both “buy” signals close to aligning, I would not be surprised to see markets make another advance higher near term. However, focusing back on longer-term market dynamics, the deviation from the longer-term mean is extreme.

Reversions always occur when least expected, and always for a reason “no one sees coming.”

With markets still in the “seasonally strong” period of the year, lots of liquidity, and plenty of exuberance, this is not a time to be “bearish” on markets.

We are using recent weaknesses to add to positions we took profits in recently, such as energy and financials. We will also add to beaten-up “growth” names that have strong earnings trajectories and strong fundamentals.

It should be evident that an honest assessment of uncertainty leads to better decisions.

The problem with “Eternal Bullishness” and “Willful Blindness” is that the failure to embrace uncertainty increases risk, and ultimately loss.

We must be able to recognize and be responsive to changes in underlying market dynamics. If they change for the worse, we must be aware of the portfolio model’s inherent risk. The reality is that we can’t control outcomes. The most we can do is influence the probability of specific outcomes.

Focusing on risk not only removes “willful blindness” from the process, but it is also essential to capital preservation and investment success over time.

In other words, “buy now,” just don’t forget to “sell” later.

Tyler Durden

Tue, 03/30/2021 – 09:15

Fed Emergency Bank Bailout Facility Usage Hits New Record High; Money Market Funds See Small…

US Homeowner Equity Drops For First Time Since 2012 The housing bull market has peaked…

JPMorgan and Citigroup Are Using the Same Accounting Maneuver as Silicon Valley Bank on Hundreds…

At Year End, 4,127 U.S. Banks Held $7.7 Trillion in Uninsured Deposits; JPMorgan Chase, BofA,…

Do you really own something if someone forces you to make never-ending (and ever-increasing) payments…

Doug Casey On Why The US Is Headed Into Its 'Fourth Turning' Authored by Doug…

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}