With Fed’s Reverse Repo Hitting Half A Trillion, Wall Street Scrambles To Figure Out What Comes Next

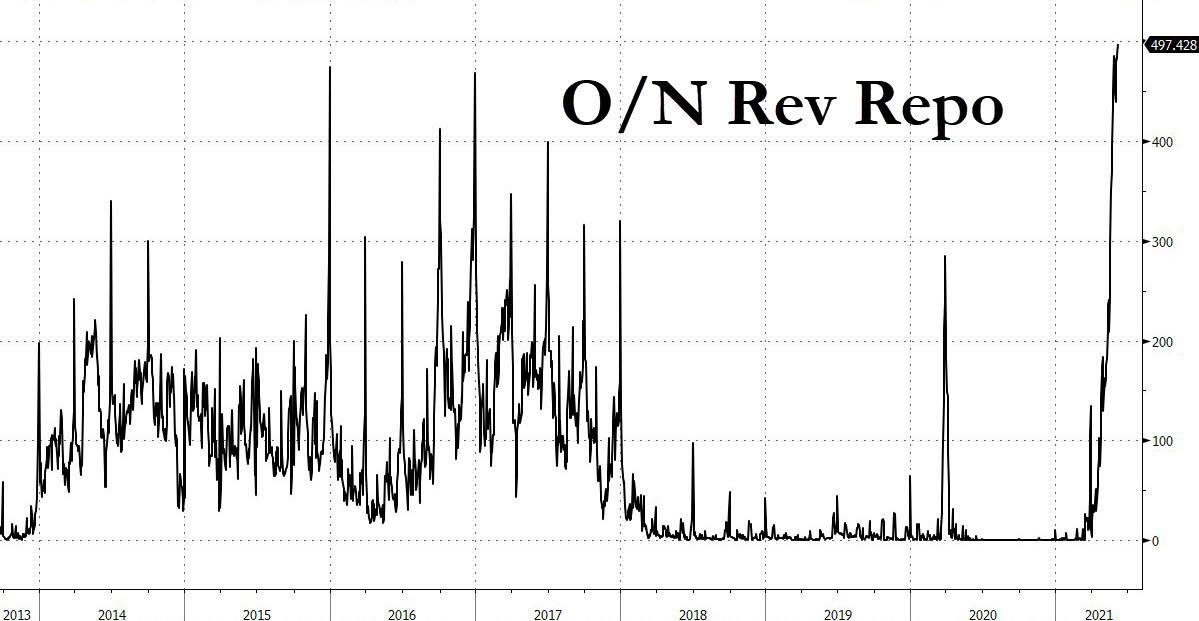

With usage of the Fed’s overnight reverse repo facility again hitting a new record high on Tuesday, rising to an all-time high of $497.4 billion…

… rates traders are trying to decide if the Fed will tweak the rate on either the IOER (Interest on Excess Reserves) or the Reverse Repo Facility, collectively the Fed’s "administered rates" in order to ease the liquidity congestion that has parked half a trillion dollars at the Fed where it is sitting inert, doing nothing.

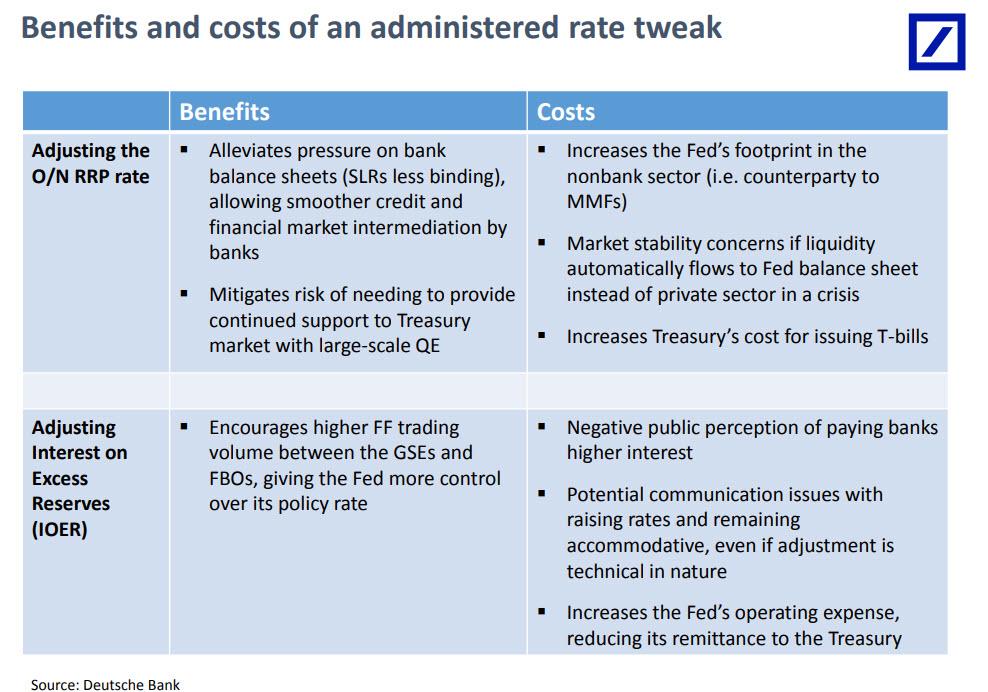

One strategist who believes there is a "small chance" the Fed will adjust its IOER/RRP rate is Deutsche Bank’s Steven Zeng, who also cited concern about the quarter-end balance sheet squeeze, which is less than the futures market is currently pricing.

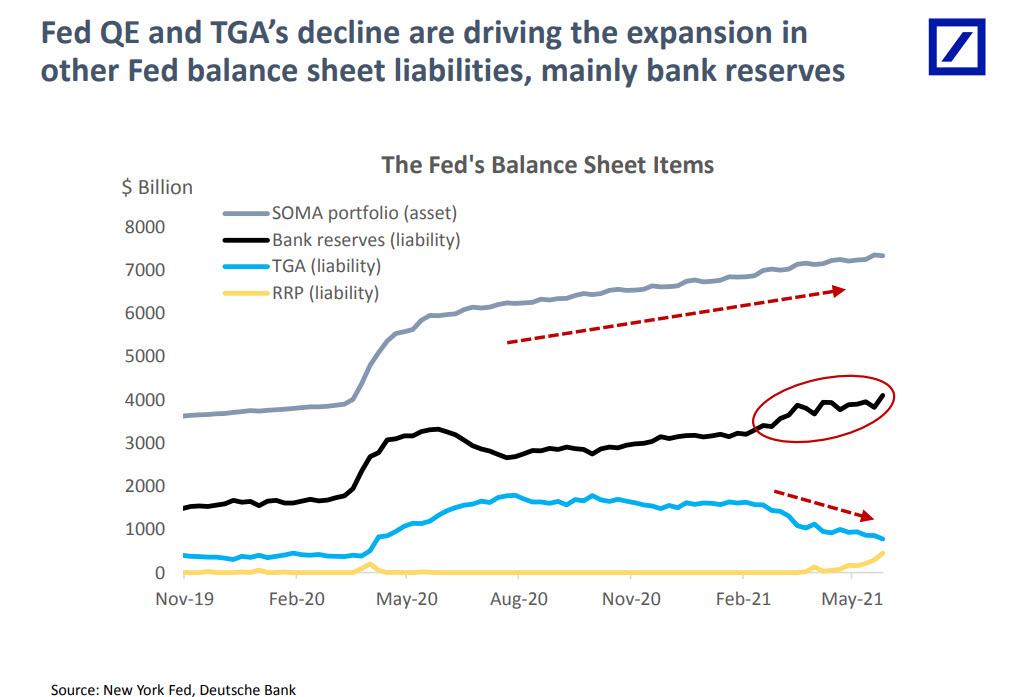

As a reminder, the Fed’s ongoing $120BN in monthly QE and Treasury’s continued drawdown of its cash balance, create permanent reserves that are sitting on bank balance sheets.

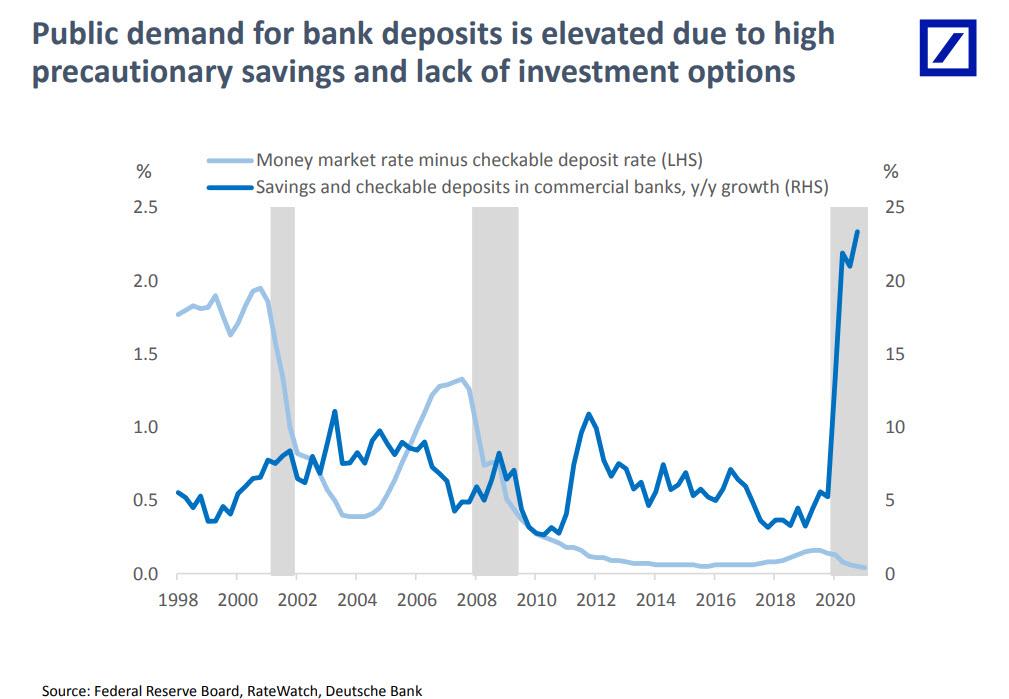

At the same time, demand for deposits adds to the bloat and forces banks to supply these liabilities and hold lower-yielding assets.

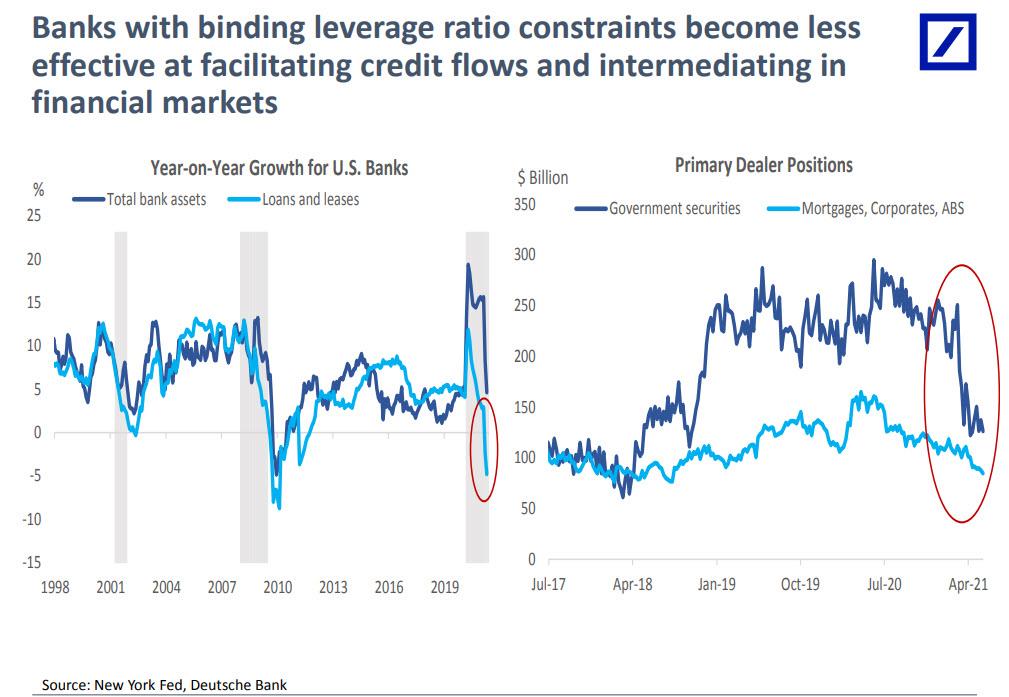

This puts downward pressure on banks’ supplementary leverage ratios, so now institutions must either raise capital or reduce loans. In this context, the Fed’s RRP acts as a “release valve” for deposits to leave banks’ balance sheets via inflows into money funds, which are then deposited at the facility.

According to Zeng, and as we have explained previously, the main merit of raising the RRP rate is to make money funds a “more attractive option to bank deposits,” which can allow institutions to push out more deposits and better manage their balance-sheet size until a “more permanent change to bank capital rules is made.”

Currently, money-market yields are low and their margins are squeezed, so a boost to the RRP rate would make money funds a “more attractive option than bank deposits,” allowing more cash to leave the banking sector. Separately, JPMorgan writes that most money-market funds have not reached their counterparty limits at the Federal Reserve’s overnight reverse repurchase agreement facility so they may not have to adjust their thresholds at the moment.

Of course, one can’t have an increase in one rate without the other, since in the fed funds market, lenders who have access to the RRP will demand higher rates, but borrowers may respond with reduced demand leading to a “more erratic fed funds rate.” This means an increase in the RRP rate “needs to be accompanied by an equal or larger increase to the IOER.”

Zeng conveniently summarizes the costs and benefits of an administered rate tweak in the table below:

On the other end of the spectrum are Jefferies economists Thomas Simons and Aneta Markowska who pointed to recent rise in yields at Treasury bill auctions in anticipation of potential Federal Reserve adjustments to its adminstered rates, but according to the duo, "the rise could compel the central bank to stay put." (earlier this week, the Treasury sold 3-month bills at 0.025% and 6-month bills at 0.04%, which were both the highest stopout yields since April 19).

Simons and Markowska explain the reflexive paradox as follows: "concerns about an IOER hike are preventing yields from falling any further, despite the huge amount of cash looking for a home in the front-end." As a result, "perversely, this concern may actually prevent an IOER hike, should yields continue to hover at these levels.”

Another paradox: the two conclude that "it is hard to see the Fed judging that there is ‘undue pressure’ on the front-end even" even as the Fed reverse repo is expected to rise above $500 billion today.

So what does the market think? Well, according to Curvature’s repo guru Scott Skyrm, as of this moment the market does not appear to be expecting an IOER hike by the Fed next week, meaning that consensus expected Powell & Co. to do nothing to ease the record liquidity parked at the Fed.

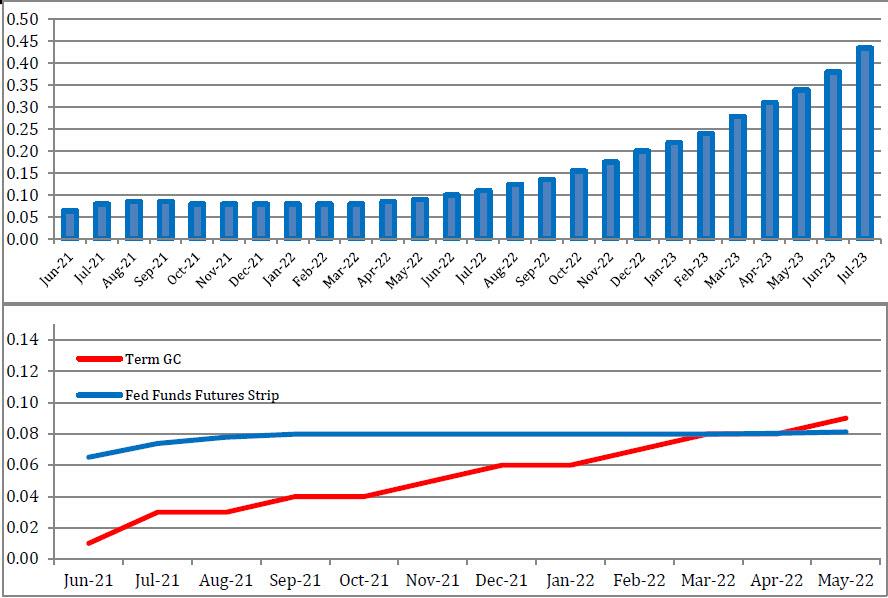

As the Curvature strategist wrote in a Tuesday note, "the market is pricing two things from the Fed. First, it’s pricing the first tightening in 2023 – according to the fed funds futures contracts [graph upper right]. Too far out to even guess the month! Second, the market is pricing the GC/fed funds spread to gradually narrow over the next year. Whereas GC is averaging between 5 and 6 basis points below fed funds now, it’s expected to trade flat to fed funds within a year."

As Skyrm concludes, "there are only two possible Fed "technical adjustments" that can raise Repo rates: QE tapering and an RRP rate increase. An increase in the IOER would raise both fed funds and Repo GC, so we could say the market is NOT pricing an IOER increase."

One final reason why the Fed is almost guaranteed to do nothing to administered rates and allow the liquidity glut to keep rising is that as the Fed’s new whisperer at the WSJ, Michael Darby wrote yesterday "Fed Is Fine With Reverse Repos Nearing Half a Trillion " in which he wrote:

Many market participants have looked at the reverse repo activity with some unease. Financial firms have been willing to take the zero percent the Fed offers them through the facility in large part because there are few other short-term investments available, and in some cases, these private market investments actually cost money to invest in. That makes the Fed’s zero percent repo rate attractive on a relative basis.

“The system is working exactly as designed,” New York Fed President John Williams said in a video interview on Yahoo Finance last Thursday. The reverse repo facility, he added, is “working really well and the fact that funds are flowing between the banking system and our overnight reverse repos, this is kind of how we would expect that to happen” given the level of money coursing through short-term markets.

The growing use of the reverse repo facility follows Lorie Logan, who manages the Fed’s massive $7.9 trillion holdings of cash and securities, having said recently that the central bank would rely on it more and expand the number of firms that could access it. The timing of that shift lined up with the wall of cash that started flowing to the Fed.

What is happening at the reverse repo facility doesn’t have much of a broader economic impact. Meanwhile, central bankers have become confident enough in the general health of financial markets to debate pulling back on their $120 billion a month in bond buying stimulus.

But as confident as the NY Fed’s career academic head, Williams, is, some expert market participants are anxious. “That amount of cash flowing into the Fed is not healthy for the repo market,” said the abovementioned Scott Skyrm; He thinks the Fed needs to scale back its bond purchases, which he deemed the “most obvious and most effective way to bring cash back into the market” and out of the Fed’s balance sheet.

Alas, it now appears that won’t happen. And so, with the Fed facility set to keep rising, the question is will we hit $1 trillion in inert liquidity at the Fed before the Fed does agree that someone is wrong, or will an amount of cash greater than the market cap of bitcoin and ethereum remain frozen inside some Fed server…

Tyler Durden

Wed, 06/09/2021 – 11:46